Looking Ahead This Week

With the Federal Reserve’s rate decision now behind us—and Jerome Powell having delivered what was his final meeting as Chair—attention turns to what the incoming leadership of Kevin Warsh will mean for monetary policy direction in the second half of 2026. The transition at the Fed arrives at a delicate moment: inflation remains above target, the energy situation is unresolved, and the FOMC’s unusually divided April vote—eight-to-four, the most dissents since October 1992—signals meaningful internal disagreement over the path forward. Markets will be listening closely for any early signals from Warsh on rate philosophy and Fed independence.

The April Consumer Price Index report, due this week, is one of the most consequential data releases of the year. After March CPI spiked to 3.3% on the back of war-driven energy costs, April’s reading should capture the first meaningful benefit of the oil price retreat that followed the ceasefire announcement—but the renewed climb in crude toward and above $100 per barrel in recent weeks complicates that picture. Core inflation’s trajectory will be the Fed’s primary focus. Q1 earnings season is also entering its most data-rich stretch, with a large number of S&P 500 companies still to report results. With the earnings beat rate running above 84% and the growth rate tracking toward 21% above estimates, the bar for further upside surprises is rising. OPEC+’s recent decision to announce a symbolic production increase during the Strait of Hormuz closure deserves close monitoring, as any meaningful shift in oil supply signals will have outsized consequences for both energy prices and inflation expectations heading into the summer.

Economic Data and Market Highlights: Week of April 28, 2026

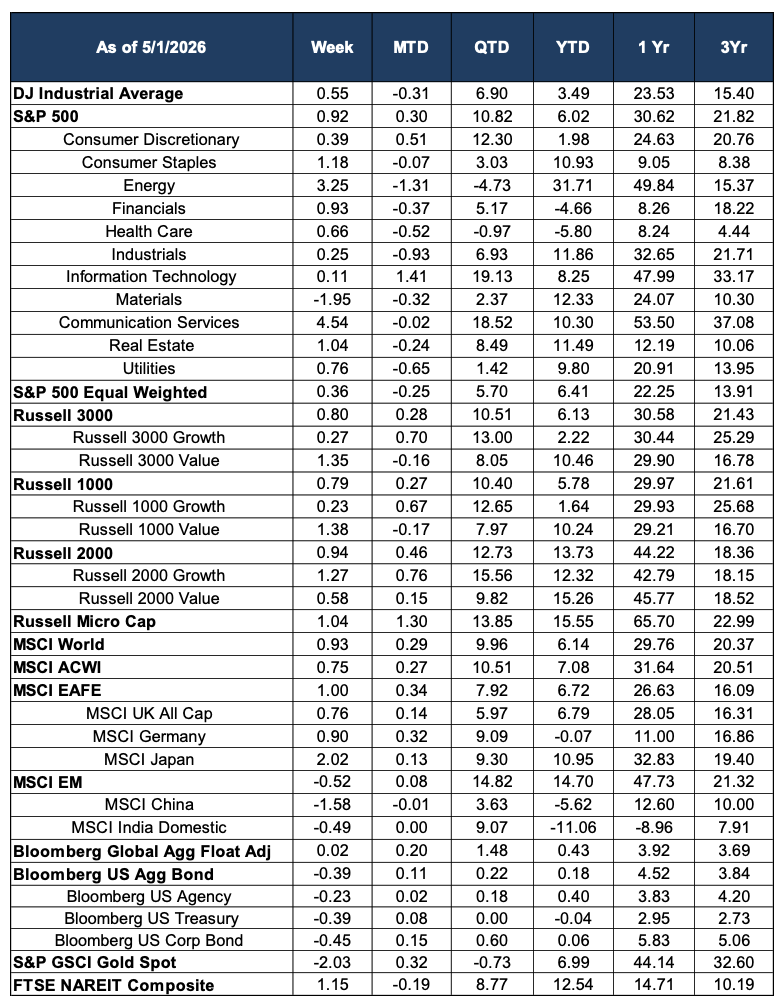

U.S. equity markets continued their advance during the week ending May 1, 2026, with the S&P 500 gaining 0.92% and the Dow Jones Industrial Average adding 0.55%, as strong mega-cap technology earnings and a broadly steady Federal Reserve decision offset renewed energy market uncertainty. The S&P 500 now stands at +6.02% year-to-date, extending a recovery that has taken the index from near-correction territory in mid-March to fresh all-time highs in just seven weeks. The week’s single most important earnings report came from Apple, which posted fiscal second-quarter revenue of $111.2 billion—up 17% year-over-year—against analyst expectations of $109.7 billion, with earnings per share of $2.01 beating the $1.96 consensus. Apple’s guidance for the June quarter was especially striking, calling for revenue growth of 14–17% versus the 9.5% the Street had anticipated, sending shares up more than 3% and lifting the broader Communication Services and Technology complex.

The Federal Reserve’s April 28–29 FOMC meeting concluded as expected with rates held steady at 3.50%–3.75%, but the internal dynamics were more consequential than the outcome. The vote split eight-to-four—the largest number of dissents since October 1992—reflecting deep disagreement among Committee members over the appropriate balance between an inflation environment still running above target and a labor market that has shown recent signs of softening. In what is now confirmed as his final meeting as Chair, Jerome Powell stated he would remain on the Board of Governors while a separate institutional investigation concludes, preserving continuity at the Fed during the transition to Kevin Warsh.

Macro Backdrop: Energy Keeps Markets on Edge

The oil market continued to reassert itself as a primary macro variable. Exxon Mobil’s CEO warned publicly that markets have not yet fully priced the impact of the Iran war on global supply, a statement that carries weight given the company’s visibility into physical oil flows. OPEC+ added to the complexity by announcing a symbolic production increase during the Strait of Hormuz closure—a move that is more political signal than material supply relief, given that the primary constraint remains the closure of the strait rather than production capacity. U.S. retail gasoline prices hit $4.39 per gallon in their largest single-day jump since the ceasefire was announced, a direct political and economic pressure point that is being closely monitored by the administration. Against this backdrop, the Energy sector gained another 3.25% on the week and the energy complex broadly remains the year’s most powerful structural theme.

Domestic Equities

Sector performance for the week reflected a market finding its footing at elevated levels, with gains spread across most sectors but leadership rotating away from the pure technology names that had dominated the prior weeks. Communication Services led all sectors with a gain of 4.54%, powered by Apple’s earnings-driven rally and strength in other mega-cap names including Meta and Alphabet. Consumer Staples rose 1.18%, Real Estate added 1.04%, and the Russell Micro Cap gained 1.04%. Energy gained 3.25% on continued oil price support. Financials added 0.93%, Health Care recovered modestly at +0.66%, and Utilities rose 0.76%.

The week’s notable underperformer was Materials, which declined 1.95%, giving back some of its recent outperformance as commodity pricing dynamics shifted. Information Technology was essentially flat at +0.11%, a marked contrast to its dominant role in recent weeks and a signal that the semiconductor rally may be entering a consolidation phase after its extraordinary run. Industrials rose a muted 0.25%.

Year-to-date, the sector divergences remain striking. Energy leads all sectors at +31.71%, followed by Materials at +12.33%, Consumer Staples at +10.93%, Industrials at +11.86%, and Real Estate at +11.49%. At the other end, Health Care is down 5.80% and Financials are off 4.66%, reflecting the persistent headwinds from Medicaid and Medicare policy changes and the uncertain rate environment, respectively. The S&P 500 Equal Weighted index gained a more modest 0.36% on the week but has been the beneficiary of the broadening market participation seen since early April, now up 6.41% year-to-date compared to the cap-weighted index’s 6.02%.

International Equities

International markets delivered broadly positive results for the week, with developed market equities showing renewed resilience after their difficult prior week. The MSCI EAFE gained 1.00% and now stands at +6.72% year-to-date. Japan was the standout developed market performer, with the MSCI Japan advancing 2.02% on the week and extending its year-to-date gain to +10.95%—one of the stronger major market performances globally. Germany rose 0.90%, essentially erasing its year-to-date deficit to arrive at -0.07% for the year. The UK added 0.76%. The MSCI World gained 0.93% and the MSCI ACWI advanced 0.75%.

Emerging markets gave back a modest 0.52% on the week, with China declining 1.58% and remaining negative year-to-date at -5.62%, while India slipped 0.49% and continues to carry a year-to-date loss of 11.06% as it works through structural challenges. Despite the weekly dip, the MSCI EM remains the best-performing major equity region of 2026 at +14.70% year-to-date, a testament to the powerful tailwind that lower oil prices have provided to energy-importing emerging economies during the periods of ceasefire-driven relief.

Fixed Income

Fixed income markets faced modest pressure during the week, as the combination of the Fed’s hawkish hold, renewed energy price concerns, and a risk-on equity environment weighed on duration assets. The Bloomberg U.S. Aggregate Bond Index fell 0.39% on the week, pulling its year-to-date return down to a slim positive of +0.18%. U.S. Treasuries declined 0.39% and corporate bonds gave back 0.45% as spreads widened slightly. The Bloomberg Global Aggregate Float Adjusted index was essentially flat, gaining a marginal 0.02%. While the weekly performance was slightly negative, the year-to-date fixed income picture remains constructive relative to the depth of pressure seen earlier in the year, and the asset class continues to provide meaningful diversification benefit in a geopolitically volatile environment.

Alternatives & Commodities

Gold pulled back 2.03% on the week but retains a substantial year-to-date gain of +12.54% and a one-year return of +44.14%, reflecting the depth of its structural bid throughout the year. The weekly decline likely reflects profit-taking following an extended run and some modest reduction in immediate safe-haven demand, but the fundamental drivers—central bank accumulation, inflation hedging, and geopolitical uncertainty—remain fully intact. Real estate investment trusts continued their recovery, with the FTSE NAREIT Composite gaining 1.15% on the week and extending its year-to-date return to +12.54%, benefiting from the improving economic backdrop and expectations that any future rate easing will be supportive of property valuations.

Source: Morningstar. Market data as of May 1, 2026. Economic and news data sourced from CNBC, Al Jazeera, Fox Business, FactSet, NBC News, and Apple Investor Relations. Past performance is not indicative of future results. This commentary is for informational purposes only and does not constitute investment advice.