Looking Ahead This Week: May 18, 2026

Markets enter the week of May 18 with a recalibrated set of expectations following a hotter-than-anticipated April inflation report. With the Federal Reserve’s rate-cut path now effectively priced out through the end of 2027, investor attention turns to Nvidia’s earnings on May 20 — a critical bellwether for the AI investment cycle and the broader technology sector. Fed speakers are likely to set a cautious tone as policymakers digest the CPI surge, while housing starts and building permits data may offer clues about how elevated borrowing costs are affecting the real economy.

The energy market remains volatile with Brent crude trading near multi-year highs as the Strait of Hormuz partial closure continues to constrain global supply. Consumer-facing companies face a challenging backdrop, as the University of Michigan’s preliminary consumer sentiment reading for May reached an all-time low, raising questions about the durability of domestic spending. Investors will need to weigh the resilience of mega-cap growth against a backdrop of tightening financial conditions, softening consumer confidence, and persistent geopolitical risk.

Economic Data and Market Highlights: Week of May 11, 2026

Macro Backdrop

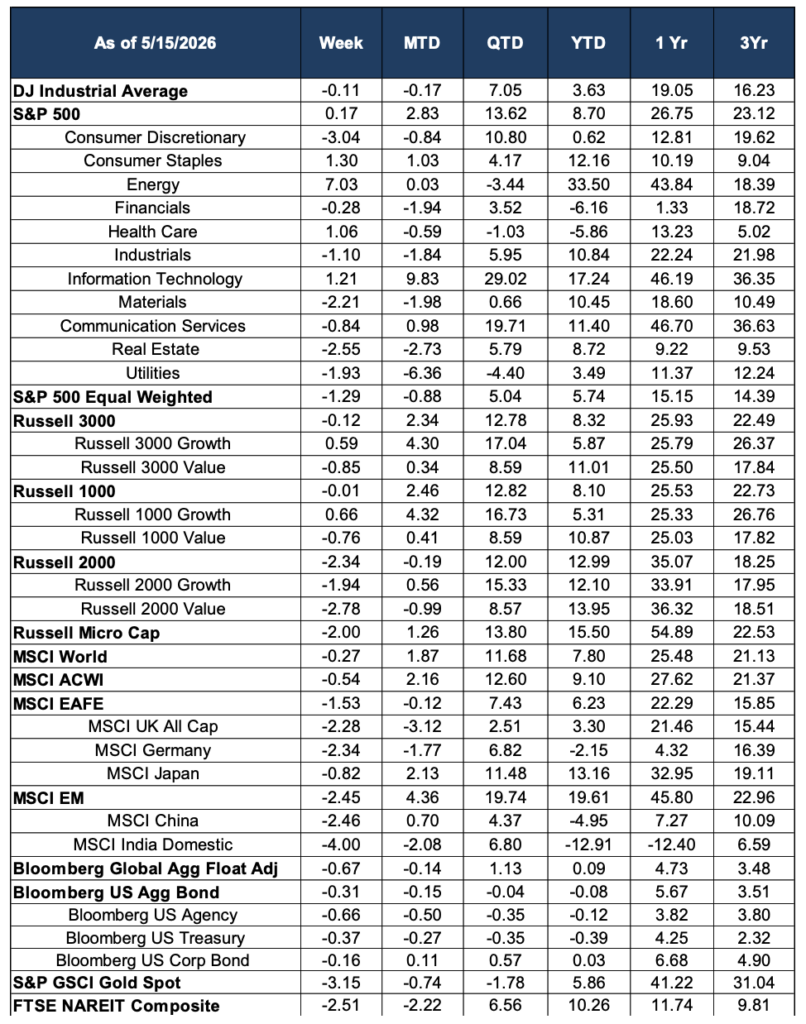

The week’s defining event was the release of April CPI data on May 12, which showed consumer prices rising 3.8% year-over-year — the hottest reading since May 2023 and well above the Federal Reserve’s 2% target. The monthly gain of 0.6% was driven significantly by energy prices, which climbed 3.8% for the month and 28.4% on an annual basis, reflecting the ongoing supply shock stemming from the effective closure of the Strait of Hormuz. Core CPI, excluding food and energy, rose 0.4% monthly and 2.8% annually. The data prompted markets to reprice rate cut expectations dramatically, with traders now assigning virtually zero probability to rate reductions through the end of 2027, and odds of a rate hike climbing to roughly 39% following a similarly elevated PPI reading on May 13.

Retail sales data released mid-week painted a picture of a consumer under strain, with notable pullbacks in furniture (-2.0%), clothing (-1.5%), and department stores (-3.2%), as higher energy and food costs absorbed more household budgets. The University of Michigan’s preliminary consumer sentiment reading for May hit an all-time low, a stark warning sign for second-half consumption and a reminder that the real-economy costs of energy supply disruptions extend well beyond the pump.

Domestic Equities

The S&P 500 eked out a narrow weekly gain of +0.17%, masking a turbulent week that featured new record highs early in the session before a Friday selloff driven by inflation fears and rising Treasury yields. The index closed near 7,501 — still elevated on a year-to-date basis at +8.70% — but the breadth of the market told a more cautious story. The equal-weighted S&P 500 fell -1.29% for the week, and small-cap benchmarks declined sharply, with the Russell 2000 off -2.34% and Russell Micro Cap down -2.00%, suggesting investors rotated toward larger, more defensible names.

Energy was far and away the week’s standout sector, surging +7.03% as oil prices held near multi-year highs driven by Middle East supply constraints and tight global inventories; the sector now leads all S&P 500 sectors year-to-date at +33.50%. Information Technology also held positive ground, gaining +1.21%, supported by continued AI spending optimism ahead of Nvidia’s May 20 earnings report. Consumer Discretionary was the week’s worst performer, falling -3.04% amid weak retail sales data and deteriorating consumer confidence. Utilities (-1.93%), Real Estate (-2.55%), and Materials (-2.21%) also declined as the prospect of higher-for-longer interest rates weighed on yield-sensitive and cyclically exposed names.

International Equities

International developed markets pulled back, with the MSCI EAFE declining -1.53% for the week. European benchmarks were notably weak, as MSCI Germany fell -2.34% and MSCI UK All Cap dropped -2.28%, reflecting a combination of slowing euro-area growth and heightened sensitivity to elevated energy import costs. Japan was relatively resilient, with MSCI Japan declining just -0.82%, supported by ongoing corporate governance reforms and a weaker yen providing continued export support.

Emerging markets also retreated, with the MSCI EM index down -2.45% on the week. MSCI China fell -2.46% and MSCI India Domestic declined -4.00%, the latter weighed down by surging energy import costs that widened India’s trade deficit in April by more than analysts had forecast. Despite the weekly pullbacks, MSCI EM remains the top-performing major region year-to-date at +19.61%, and longer-term structural tailwinds across key emerging economies remain intact.

Fixed Income

The hot April CPI reading pushed Treasury yields higher across the curve, pressuring bond prices and delivering modest losses to most fixed income categories. The Bloomberg US Aggregate Bond Index declined -0.31% for the week and remains essentially flat on the year (-0.08% YTD). Bloomberg US Treasury was down -0.37% on the week and -0.39% YTD as rate-hike odds re-entered market discourse. Investment-grade corporate bonds held up comparatively better, with the Bloomberg US Corporate Bond Index declining only -0.16%, supported by relatively stable credit spreads. Global bonds also softened, with the Bloomberg Global Aggregate Float Adjusted Index falling -0.67% on the week.

The evolving interest rate environment — where a Fed on hold increasingly resembles a Fed considering tightening — continues to make duration management a central challenge for fixed income allocators. With rate cuts priced out and hike probabilities creeping higher, the case for shorter-duration postures and credit selectivity remains compelling.

Alternatives & Commodities

Gold gave back recent gains, with the S&P GSCI Gold Spot falling -3.15% on the week, likely reflecting a rotation away from haven assets as equity markets remained near record highs early in the period, compounded by a stronger dollar response to the inflation data. Despite the weekly decline, gold remains up +5.86% year-to-date and continues to offer meaningful portfolio diversification over longer horizons, with a one-year return of +41.22%.

Energy continued its dramatic 2026 run; the sector’s +7.03% weekly gain lifted its year-to-date return to +33.50%, reflecting persistent elevated oil prices amid ongoing Middle East supply disruptions and a global inventory draw of approximately 8.5 million barrels per day in the second quarter. Real estate investment trusts retreated -2.51% for the week (FTSE NAREIT Composite), as higher-for-longer rate expectations dampened sentiment in rate-sensitive real assets, though the sector remains up +10.26% year-to-date.

Source: Morningstar. Market data as of May 15, 2026. Past performance is not indicative of future results. The information provided is for educational and informational purposes only and does not constitute investment advice.