Economic Data and Market Highlights

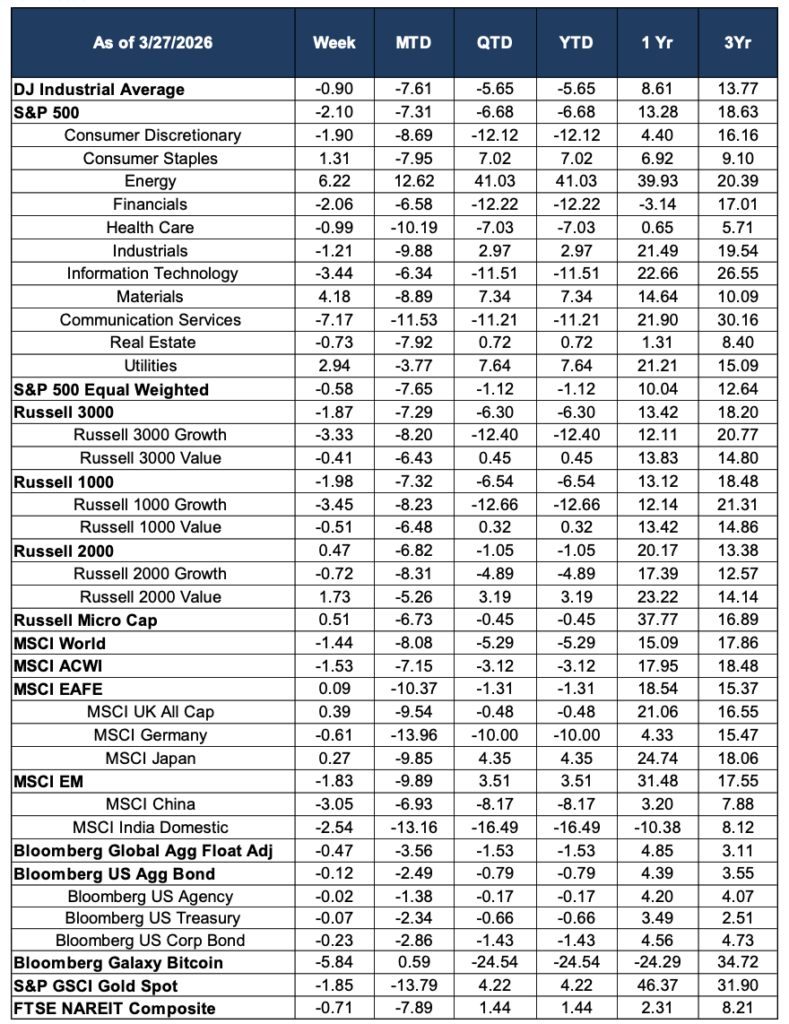

Global equity markets suffered another bruising week ending March 27, 2026, notching a fifth consecutive weekly loss—the longest losing streak since 2022—as surging oil prices, mounting recession fears, and a dramatically repriced interest rate outlook combined to rattle investor confidence. The Dow Jones Industrial Average declined 0.90% on the week and has now slipped into correction territory, down 5.65% year-to-date, while the S&P 500 fell further to sit approximately 9% below its late-January record high of 6,978. The escalating conflict in the Middle East, with Brent crude surging above $112 per barrel following new attacks on Iranian energy infrastructure and fears of a prolonged Strait of Hormuz disruption, dominated market narrative. President Trump set an April 6 diplomatic deadline for Iran, making that date the single most consequential near-term variable in the global macro outlook.

Macro Backdrop: Stagflation Fears and Rising Recession Odds

The macro environment darkened considerably this week as a confluence of indicators pointed toward the possibility of stagflation—a combination of slowing growth and persistent inflation that central banks are poorly equipped to address. Recession probability estimates from major forecasters rose sharply: Goldman Sachs lifted its odds to 30%, Moody’s Analytics placed them near 50%, and EY Parthenon and Wilmington Trust put their estimates at 40% or higher. The catalyst was a deteriorating labor market, with the unemployment rate rising to 4.4% and the economy posting its first notable monthly job loss since the pandemic era.

At the same time, oil prices near $112 per barrel are feeding directly into headline inflation readings, and the bond market delivered a stark warning: the 10-year Treasury yield climbed to 4.44%, its highest level since July 2025, while the 2-year yield settled at 3.88% and the 30-year reached 4.98%. Most strikingly, futures markets have begun pricing in a greater-than-50% probability of a Federal Reserve rate hike by year-end—the first time that threshold has been crossed—reflecting concern that the energy shock could force the Fed’s hand even as growth slows. The combination of tighter financial conditions, higher commodity prices, and trade policy uncertainty creates a particularly challenging backdrop for risk assets.

Domestic Equities

Domestic sector performance this week was among the most extreme of the year, reflecting the oil price shock in vivid terms. Energy surged 6.22% on the week and has now extended its year-to-date gain to an extraordinary +41.03%, a remarkable divergence from virtually every other segment of the market. Materials also rose 4.18%, benefiting from commodity price momentum. Every other sector declined. Communication Services led losses with a steep drop of 7.17%, followed by Utilities at -5.44% and Health Care at -3.44%. Information Technology fell 2.71%, bringing its year-to-date loss to -7.11%, while Consumer Discretionary declined 2.10% and now sits at -12.12% for the year. Financials, already deeply negative at -12.22% year-to-date, fell another 2.06% on the week.

The breadth of selling was notable but somewhat concentrated. The S&P 500 Equal Weighted index declined just 0.58% on the week—a meaningful outperformance relative to the cap-weighted index—suggesting that large-cap growth and technology stocks faced disproportionate pressure. This dynamic is consistent with the ongoing rotation: Russell 1000 Value outperformed Russell 1000 Growth for another consecutive week, as investors continued to favor earnings stability and commodity exposure over long-duration growth stories. Small caps showed relative resilience, with the Russell 2000 declining only 0.72% on the week. Year-to-date, however, the broad picture remains difficult: the Russell 2000 is down 4.89%, the Russell 1000 is off 6.54%, and large-cap growth indices have borne the heaviest losses.

International Equities

International equity markets were mixed, with some notable divergences. Japan stood out as the lone major market to post a weekly gain, with the MSCI Japan rising 0.27% on the week; Japanese equities have benefited from a weaker yen and their own energy-exporting industrial base, and remain up 4.35% for the quarter. Germany, by contrast, fell 4.35% on the week as European industrial concerns intensified, and the index is now down 10.49% year-to-date—one of the weaker major markets globally. The UK declined a more modest 0.61%. The MSCI EAFE fell modestly overall, though the index continues to outperform U.S. large caps on a year-to-date basis.

Emerging markets showed resilience, with the MSCI EM posting a slight decline as China provided a partial offset to weakness elsewhere. India continued its difficult stretch but appears to be finding some stabilization. The MSCI ACWI fell 1.53% on the week and is now down 3.12% year-to-date. The outperformance of international equities relative to U.S. markets remains one of the defining portfolio themes of 2026, reinforcing the value of geographic diversification in a fragmented geopolitical environment.

Fixed Income

Fixed income markets faced renewed pressure as yields rose sharply across the curve. The Bloomberg U.S. Aggregate Bond Index declined 0.12% on the week and is now down 1.43% year-to-date, reflecting the dual headwinds of inflation-driven yield increases and widening credit spreads. The Bloomberg Global Aggregate Float Adjusted index fell 0.47%. Corporate bonds underperformed Treasuries as credit spreads widened in response to rising recession concerns. The inversion of the rate-cut narrative—with markets now contemplating rate hikes rather than cuts—has fundamentally altered the fixed income backdrop, and the 10-year yield at 4.44% represents a meaningful headwind for duration-sensitive assets including bonds and rate-sensitive equity sectors.

Alternatives & Commodities

Gold continued to assert its role as the preeminent safe-haven asset of the current cycle. The S&P GSCI Gold Spot index advanced again this week, pushing its year-to-date return to approximately +22%, and its twelve-month gain now stands among the strongest of any major asset class. The combination of geopolitical risk, inflation concerns, and growing institutional demand for non-correlated stores of value has made gold a standout performer in what has otherwise been a turbulent quarter. Bitcoin posted a modest gain of 1.95% on the week and remains positive year-to-date at +4.22%, though its volatility relative to gold underscores the distinct risk profiles of the two assets. Real estate investment trusts continued to struggle, with the FTSE NAREIT Composite declining 0.71% on the week as the higher-for-longer rate regime weighs on property valuations.

Looking Ahead

Markets enter the final days of Q1 2026 in a distinctly more fragile state than the year began. The April 6 diplomatic deadline between the U.S. and Iran represents the most immediate binary risk event: a de-escalation that reopens the Strait of Hormuz could rapidly reverse oil prices and alleviate much of the inflationary pressure currently gripping markets, while further escalation could push crude prices higher still and accelerate the stagflation scenario. Beyond geopolitics, investors will be focused on incoming labor market data, any further Fed commentary in light of the dramatic shift in rate expectations, and Q1 earnings season, which begins in earnest in mid-April. With valuations under pressure, earnings guidance will be scrutinized closely for any signs that the macro headwinds—tariffs, higher energy costs, and softening consumer spending—are beginning to erode corporate margins. Portfolio resilience through diversification across geographies, factor exposures, and asset classes has rarely been more important.

Source: Morningstar. Market data as of March 27, 2026. Economic and news data sourced from CNBC, CNN Business, CME Group FedWatch, FinancialContent, and Charles Schwab. Past performance is not indicative of future results. This commentary is for informational purposes only and does not constitute investment advice.