Economic Data and Market Highlights

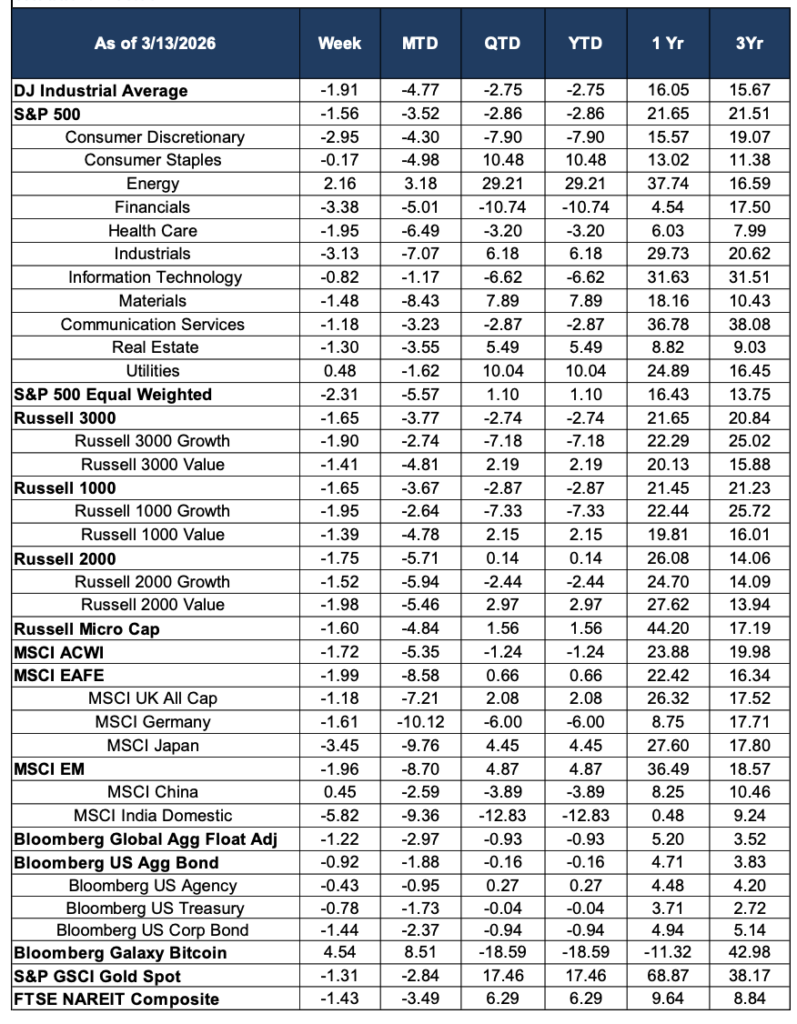

Global equity markets extended their retreat during the week ending March 13, 2026, with virtually all major indices posting losses amid continued macro uncertainty. The Dow Jones Industrial Average declined 1.91% on the week, bringing its month-to-date loss to 4.77%, while the S&P 500 fell 1.56%, pulling its year-to-date return to -2.86%. The selling pressure was broad-based but uneven, with cyclical and growth-oriented sectors bearing the brunt of the decline. Defensively positioned assets—most notably energy commodities and gold—continued to serve as relative safe havens, underscoring a risk-off tone that has characterized trading through the first quarter.

Domestic Equities

Within the S&P 500, sector performance was sharply bifurcated. Financials led declines, falling 3.38% on the week and extending their year-to-date loss to -10.74%, reflecting concerns about credit quality and net interest margin compression in a slowing growth environment. Industrials shed 3.13%, while Consumer Discretionary dropped 2.95% as consumer spending confidence wanes. Health Care and Consumer Staples also lagged the broader index. The two bright spots were Energy, which rose 2.16% on the week and remains the standout sector year-to-date at +29.21%, and Utilities, which eked out a modest gain of 0.48% and is up 10.04% for the year—both sectors reflecting classic late-cycle defensive rotation.

The S&P 500 Equal Weighted index declined 2.31%, underperforming the cap-weighted index by 75 basis points, suggesting that mega-cap names provided modest relative cushion during the selloff. The growth-versus-value dynamic continued to favor value: within the Russell 1000, value fell 1.39% compared to a 1.95% decline for growth. Small caps were not spared, with the Russell 2000 dropping 1.75% on the week, though its year-to-date return remains essentially flat at +0.14%. The Russell Micro Cap index declined 1.60% for the week but maintains a year-to-date gain of 1.56%.

International Equities

International markets were also under pressure, with the MSCI ACWI declining 1.72% on the week. Developed market equities, as measured by the MSCI EAFE, fell 1.99%, with Japan the notable laggard among major markets at -3.45% for the week and -9.76% month-to-date. Germany declined 1.61% on the week and remains down 6.00% year-to-date, while the UK was comparatively resilient at -1.18%. Despite near-term weakness, developed international markets have held up reasonably well on a year-to-date basis, with MSCI EAFE up 0.66%—a meaningful contrast to U.S. large-cap indices, which are modestly negative for the year.

Emerging markets declined 1.96% for the week, though year-to-date returns remain positive at +4.87%. India was the weakest major emerging market, falling 5.82% on the week and extending its year-to-date loss to -12.83%—a notable reversal from prior-year strength. China was the lone bright spot across international equity markets, gaining 0.45% on the week, though it remains down 3.89% year-to-date.

Fixed Income

Fixed income markets also saw modest declines, with the Bloomberg U.S. Aggregate Bond Index falling 0.92% on the week and down 0.16% year-to-date. Corporate bonds were the weakest component, with the Bloomberg U.S. Corp Bond index declining 1.44% on the week, likely reflecting spread widening amid equity volatility. U.S. Treasuries held up better, declining just 0.78%, while Agency debt fell 0.43%. Globally, the Bloomberg Global Aggregate Float Adjusted index dropped 1.22% for the week, essentially flat at -0.93% year-to-date.

Alternatives & Commodities

Gold remained a standout performer on a longer-term basis despite a modest weekly pullback of 1.31%. The S&P GSCI Gold Spot index is up 17.46% year-to-date and an extraordinary 68.87% over the past twelve months, reflecting sustained demand for safe-haven assets. Real estate investment trusts, as measured by the FTSE NAREIT Composite, slipped 1.43% on the week and are up 6.29% year-to-date. Bitcoin posted a notable rebound, gaining 4.54% on the week, though the Bloomberg Galaxy Bitcoin index remains down 18.59% year-to-date following a difficult start to 2026.

Looking Ahead

The first quarter of 2026 has painted a clear picture: investors are rotating away from growth and cyclical risk toward defensives, commodities, and international diversification. Energy and utilities lead domestic sectors by a wide margin year-to-date, while technology and financials have been notable laggards. Gold’s continued strength and the resilience of international developed markets relative to U.S. equities suggest that portfolio diversification remains a meaningful tailwind. Market participants will be watching closely for any shifts in monetary policy signals, trade policy developments, and corporate earnings guidance as the quarter draws to a close.