Looking Ahead This Week: June 8, 2026

After last week’s sharp selloff, markets will be tested early by the Federal Reserve’s June policy meeting, with the FOMC rate decision expected on June 11. Chair Kevin Warsh and the committee face a difficult backdrop: a labor market that printed 172,000 jobs in May — more than double expectations — while core inflation remains well above target at 3.3% PCE. Investors will be parsing the statement and press conference carefully for any shift in the tightening bias that emerged from the April meeting. Rate-hike odds, which climbed materially on Friday’s jobs report, make the Fed’s communication this week particularly consequential.

May CPI data, also due this week, will either validate or challenge the market’s post-jobs-report repricing. A hot inflation reading following the jobs surprise could accelerate the selloff in rate-sensitive growth stocks and further compress equity multiples. The semiconductor sector remains fragile following Broadcom’s guidance disappointment and the $1.3 trillion single-session wipeout — Nvidia’s response to the AI spending narrative will be closely watched. Iran-U.S. ceasefire negotiations continue in the background; any formal agreement and a timeline for Strait of Hormuz reopening would meaningfully alter both the inflation and growth outlook for the second half of 2026.

Economic Data and Market Highlights: Week of June 2, 2026

Macro Backdrop

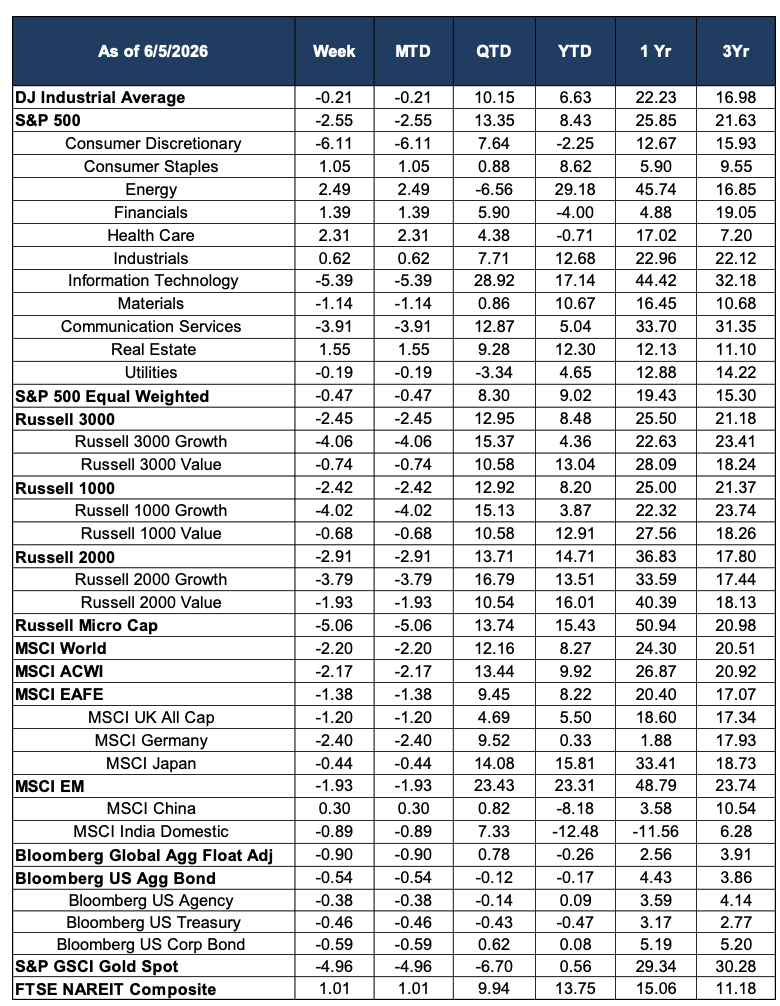

Nine weeks of consecutive gains came to an abrupt end as markets absorbed a one-two punch of earnings disappointment and a ‘good news is bad news’ jobs report. The S&P 500 fell -2.55% for the week — its worst weekly performance in months — while the Nasdaq dropped approximately 4% on Friday alone, its steepest single-day decline since April 2025. The Dow held up somewhat better, declining just -0.21%, as investors rotated into defensive and value-oriented names.

The May nonfarm payrolls report, released Friday, June 5, showed the economy added 172,000 jobs — more than double the consensus estimate of 80,000 — with the unemployment rate holding steady at 4.3%. Wage growth came in at 3.4% year-over-year, slightly below headline inflation but still above levels compatible with the Fed’s 2% price stability mandate. While the jobs data reflected genuine economic resilience, markets interpreted the strength as reducing any remaining probability of rate cuts and increasing the likelihood of further tightening. Federal Reserve Chair Kevin Warsh, who has signaled a focused anti-inflation stance since taking office, faces a difficult communication challenge at this week’s FOMC meeting given conflicting signals across the economy.

Domestic Equities

The week’s damage was concentrated heavily in growth and technology. Information Technology fell -5.39%, driven by a dramatic sector-wide selloff triggered by Broadcom’s fiscal second-quarter earnings report on June 3. Broadcom reported revenue of $22.19 billion — marginally below consensus — but the market’s reaction centered on what was not said: the company held its full-year AI semiconductor revenue forecast unchanged at $56 billion, well short of the $100 billion investors had anticipated. CEO Hock Tan’s Q3 guidance of $16 billion in AI chip revenue also fell below the $17.2 billion consensus. Broadcom shares fell approximately 15%, and the selloff cascaded across the semiconductor complex — AMD dropped nearly 11%, Intel fell over 11%, and the sector erased an estimated $1.3 trillion in market capitalization in a single session. The week served as a reminder that elevated AI valuations remain vulnerable to any shortfall in the pace of the buildout narrative.

Consumer Discretionary was the week’s worst-performing sector, falling -6.11%, as the combination of higher rate expectations, tariff concerns, and broad risk-off sentiment weighed on growth-oriented consumer names including Amazon and Tesla. Communication Services declined -3.91%, with Alphabet extending its losing streak to a fourth consecutive week. In contrast, defensive sectors performed well: Health Care gained +2.31%, Financials rose +1.39%, and Real Estate advanced +1.55% as investors sought shelter in rate-resilient and dividend-oriented names. Energy rebounded +2.49% as Iran ceasefire negotiations showed signs of stalling, partially reversing the prior weeks’ oil-price decline. The equal-weighted S&P 500 fell only -0.47% — a stark contrast to the -2.55% decline in the cap-weighted index — underscoring how concentrated the selling was in a handful of mega-cap technology names.

International Equities

International markets were not immune to the global risk-off tone, though they declined more modestly than their U.S. counterparts. The MSCI EAFE fell -1.38%, with MSCI Germany declining -2.40% and MSCI UK All Cap off -1.20%, both pressured by the global tech-driven selloff and uncertainty around the trajectory of U.S. monetary policy. MSCI Japan was comparatively resilient, falling just -0.44%, supported by ongoing structural reforms and the insulation provided by yen dynamics relative to dollar-denominated volatility.

Emerging markets declined -1.93% (MSCI EM), though the composition was nuanced. MSCI China was a rare positive, gaining +0.30% on the week and suggesting some stabilization in Chinese equities after an extended period of underperformance. MSCI India Domestic fell -0.89%, continuing to face headwinds from elevated energy import costs and currency pressure. Despite the weekly pullback, MSCI EM retains a commanding year-to-date lead at +23.31%, well ahead of all other major regional benchmarks.

Fixed Income

Fixed income markets gave back the prior week’s gains as the stronger-than-expected jobs report pushed Treasury yields higher across the curve. The Bloomberg US Aggregate Bond Index declined -0.54%, and Bloomberg US Treasuries fell -0.46%, as the market absorbed the implications of a labor market too resilient to justify any near-term Fed pivot. Bloomberg US Corporate Bond also declined -0.59%, as credit spreads widened modestly in sympathy with the broader risk-off sentiment. The Bloomberg Global Aggregate Float Adjusted Index fell -0.90% as dollar strength and rising U.S. yields spilled over into global bond markets.

The fixed income picture for 2026 remains challenging: the Bloomberg US Aggregate Bond is now down -0.17% year-to-date, and Treasuries are off -0.47% YTD. The path back to positive total returns for core fixed income depends substantially on the inflation trajectory — a scenario in which ceasefire progress reduces energy prices and PCE moderates toward 3% or below would meaningfully improve the outlook for duration assets in the second half of the year.

Alternatives & Commodities

Gold suffered its sharpest weekly decline of 2026, falling -4.96%, as the dollar strengthened on the strong jobs report and rising Treasury yields reduced the relative appeal of non-yielding assets. Despite the pullback, gold remains up +0.56% year-to-date and has returned +29.34% over the trailing twelve months — a testament to the outsized role geopolitical and inflation uncertainty has played as a tailwind for the metal throughout 2026. The sharp weekly drawdown is a reminder that gold’s safe-haven premium can compress quickly when macro catalysts shift the narrative toward growth and yield.

Energy rebounded +2.49% for the week as Iran-U.S. ceasefire talks showed signs of stalling, with unresolved disputes over deal terms and continued sporadic hostilities injecting fresh uncertainty into the oil supply outlook. Brent crude partially recovered from its multi-week decline, though it remains well below April’s highs. REITs (FTSE NAREIT Composite) rose +1.01%, one of the few areas of the market to benefit from the rotation away from growth, as investors seeking income and inflation-hedging characteristics in a volatile rate environment added real estate exposure.

Source: Morningstar. Market data as of June 5, 2026. Past performance is not indicative of future results. The information provided is for educational and informational purposes only and does not constitute investment advice.