Looking Ahead This Week: June 29, 2026

Markets enter the final week of the second quarter — and a holiday-shortened week ahead of July 4th — with the AI demand narrative under its most significant scrutiny since the sector began its extraordinary run. The question investors are wrestling with is not whether AI infrastructure spending is real, but whether the pace of that spending can continue to justify multiples that had priced in near-flawless execution through the end of the decade. Second-quarter earnings season begins in earnest in the weeks ahead, and technology management teams will face pointed questions about return on AI capital and the timeline to revenue monetization.

On the macro front, the May PCE price index — the Federal Reserve’s preferred inflation measure — is due Friday, and markets will be watching closely for any evidence that the Iran ceasefire’s disinflationary impact on energy prices is beginning to flow through to the data. A softer-than-expected print could ease the Fed’s tightening bias and provide some relief for rate-sensitive growth assets. ISM manufacturing and services data will offer a read on whether domestic economic momentum is holding in the face of higher borrowing costs and softening consumer confidence. The Great Rotation from mega-cap technology into value, small-cap, and defensive sectors continues to reshape portfolio positioning across the industry.

Economic Data and Market Highlights: Week of June 22, 2026

Macro Backdrop

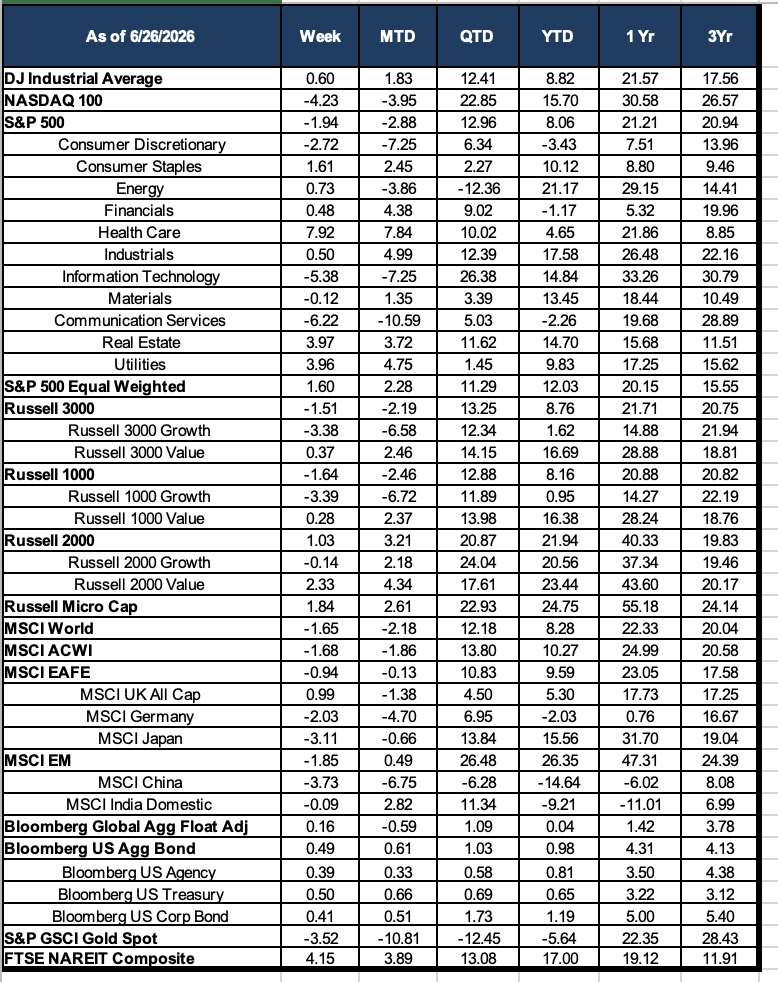

The week of June 22 delivered a second consecutive bruising week for technology and growth stocks as mounting concerns about artificial intelligence demand and capital spending discipline sent shock waves through the semiconductor and mega-cap technology complex. The S&P 500 fell -1.94% for the week while the NASDAQ 100 plunged -4.23% — its worst two-week stretch since early 2025. The catalyst this week was a combination of forces: reports that OpenAI is considering delaying its highly anticipated IPO due to market volatility in AI-related shares, an aggressive selloff in memory chip stocks globally (with Micron declining more than 10%, Marvell -8%, and international names SK Hynix and Samsung each falling more than 12%), and deepening investor concern that the extraordinary capital expenditure cycle in AI infrastructure is outpacing near-term revenue realization.

The week’s most striking market dynamic was the dramatic divergence between cap-weighted and equal-weighted equity performance. While the S&P 500 fell nearly 2%, the equal-weighted S&P 500 gained +1.60% — a spread of more than 3.5 percentage points in a single week — illustrating just how concentrated the selling has been in a handful of the largest technology names. The broad market, stripped of its mega-cap distortions, is holding up considerably better than the headlines suggest. The Great Rotation of 2026 — from AI-driven mega-cap growth into value, cyclicals, small caps, and defensives — intensified further, with defensive sectors posting some of their strongest weekly gains of the year.

Domestic Equities

Health Care was the week’s standout performer by a wide margin, surging +7.92% as investors rotated aggressively out of technology and into the sector’s combination of defensive characteristics and attractive valuations. After underperforming for much of 2026 amid the AI-driven growth narrative, Health Care names including Cardinal Health, Johnson & Johnson, and Eli Lilly surged to multi-month highs, driven by improving policy clarity on drug pricing and a fundamental re-rating as investors sought quality earnings at reasonable multiples. Utilities (+3.96%) and Real Estate (+3.97%) also posted exceptional weekly gains, benefiting both from the flight to defensives and from a decline in Treasury yields as risk-off sentiment drove demand for duration assets.

Information Technology fell -5.38% — its second consecutive week of steep losses — and Communication Services collapsed -6.22%, the worst-performing sector of the week, as Alphabet, Meta, and other mega-cap platform companies faced intensified scrutiny over their AI capital expenditure programs and near-term monetization timelines. Consumer Discretionary declined -2.72%, adding to a challenging month for the sector. The Russell 1000 Growth index fell -3.39% while Russell 1000 Value gained +0.28%, and the Russell 2000 Value index rose +2.33% — a pattern that reflects the sustained and broadening reallocation of capital from the AI-dominated growth complex into more traditional value and income-oriented investments. Small-cap indices outperformed meaningfully, with the Russell 2000 rising +1.03% and Russell Micro Cap gaining +1.84%.

International Equities

International developed markets declined modestly, with the MSCI EAFE falling -0.94% for the week. The pullback was led by MSCI Japan, which dropped -3.11% as a strengthening yen — partly driven by global risk-off flows into Japanese government bonds — weighed on export-sensitive companies. MSCI Germany declined -2.03%, reflecting both the contagion from the global tech selloff and renewed concerns about German industrial competitiveness in an era of higher energy costs, even as the Iran ceasefire gradually improves the supply outlook. MSCI UK All Cap was a relative bright spot, gaining +0.99%, supported by its heavier weighting toward value-oriented financials, energy, and consumer staples names.

Emerging markets also retreated, with the MSCI EM index falling -1.85% for the week, though the asset class continues to lead all major global regions year-to-date at +26.35%. MSCI China declined a further -3.73% and is now -14.64% year-to-date, as domestic economic headwinds and geopolitical overhang persist despite the broader ceasefire progress in the Middle East. MSCI India Domestic was essentially unchanged at -0.09%, consolidating after several volatile weeks. The EM region’s resilience on a year-to-date basis reflects the underlying strength of non-China emerging economies, where the combination of dollar weakness, commodity dynamics, and improving geopolitical sentiment has provided a sustained tailwind.

Fixed Income

Fixed income markets benefited from the risk-off rotation, with Treasuries and investment-grade bonds rallying as investors sought the relative safety of duration assets amid the equity market turbulence. The Bloomberg US Aggregate Bond Index gained +0.49% for the week, and Bloomberg US Treasuries rose +0.50%, as yields pulled back on declining risk appetite and expectations that persistent tech-driven equity weakness might give the Federal Reserve additional time before implementing any tightening. Bloomberg US Corporate Bond returned +0.41%, with credit spreads widening only modestly — suggesting markets are treating the tech selloff as a valuation correction rather than a systemic credit event.

The year-to-date picture for fixed income is improving: the Bloomberg US Aggregate Bond is now up +0.98% for the year, and Treasuries have recovered to +0.65% YTD — a meaningful turnaround from the negative territory that characterized much of the first half. If the Iran ceasefire holds and energy inflation continues to moderate, the path for additional fixed income recovery in the second half of 2026 appears more constructive than it did just a few months ago, though the FOMC’s hawkish dot plot remains a ceiling on how far rates can fall without new economic evidence.

Alternatives & Commodities

Gold continued its persistent June decline, falling -3.52% on the week and extending its month-to-date loss to -10.81%. The metal is now -5.64% year-to-date, completing a dramatic round-trip from its April highs when it stood as one of 2026’s best-performing assets. The sustained gold weakness reflects the combination of rising real yields (driven by the hawkish FOMC pivot), a stronger U.S. dollar, and the market’s recalibration of geopolitical risk premium as the Iran ceasefire extends. Despite the sharp quarterly drawdown (-12.45% QTD), gold retains a strong trailing twelve-month return of +22.35%, a reminder of how significant the safe-haven bid was during the peak of the Middle East conflict.

Real estate investment trusts were among the week’s clear winners, with the FTSE NAREIT Composite surging +4.15% as falling Treasury yields and the rotation into defensive income-producing assets created a highly favorable short-term environment. REITs are now up +17.00% year-to-date, making them one of the better-performing asset classes in 2026. Energy rebounded modestly at +0.73%, as the physical process of reopening the Strait of Hormuz proved slower than markets initially anticipated, providing some support for oil prices. The Energy sector, despite its -12.36% QTD decline, remains the top-performing S&P 500 sector year-to-date at +21.17% — a testament to how severe and sustained the supply shock of early 2026 truly was.

Source: Morningstar. Market data as of June 26, 2026. Past performance is not indicative of future results. The information provided is for educational and informational purposes only and does not constitute investment advice.