Looking Ahead This Week: July 6, 2026

Markets open the first full trading week of the third quarter with the Federal Reserve’s policy calculus significantly altered by last Thursday’s dramatically weak June jobs report. With only 57,000 payrolls added in June — barely half the consensus estimate — and prior months revised lower, the hawkish pivot signaled by the June dot plot is under immediate scrutiny. Chair Warsh’s second FOMC meeting is scheduled for July 28-29, and investors will be watching every piece of incoming data for clues about whether the committee moderates its tightening bias or presses ahead in the face of softening labor market conditions.

The more immediate focus this week will be the unofficial start of second-quarter earnings season, with the major money center banks — JPMorgan Chase, Wells Fargo, and Citigroup — typically reporting in the second week of July. Bank earnings will be closely watched for signals on consumer credit quality, loan demand, and net interest margin trends in a higher-for-longer rate environment. June CPI, also due this week, will either reinforce or complicate the Fed’s recalibration: a softer reading, combined with the weak jobs print, could mark a genuine turning point in the inflation-and-rates narrative that has dominated 2026. The technology sector’s ability to find a floor after two consecutive brutal weeks of selling — and ahead of major tech earnings in late July — will also be a key test of market conviction.

Economic Data and Market Highlights: Week of June 30, 2026

Macro Backdrop

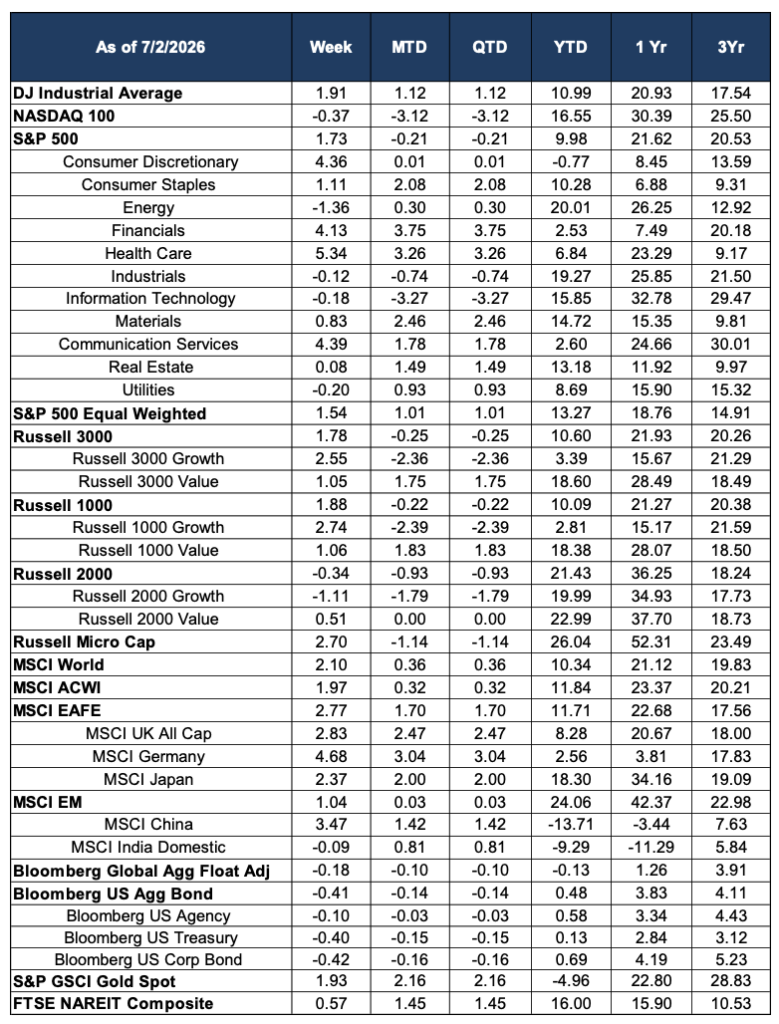

The holiday-shortened week of June 30 through July 2 — with U.S. markets closed Friday in observance of Independence Day — delivered the most consequential labor market surprise of 2026. The June nonfarm payrolls report, released Thursday July 2, showed the economy added just 57,000 jobs, missing the consensus estimate of approximately 110,000 by nearly half. Prior months were also revised lower, with May’s gain cut to 129,000 from 172,000 and April revised to 148,000 from 179,000. The unemployment rate held at 4.2%, but the trend in job creation has clearly decelerated sharply from the strong readings earlier in the year. The policy-sensitive 2-year Treasury yield fell approximately 3.5 basis points on the print, and rate-hike odds for September were effectively removed from market pricing.

The report arrived just two weeks after the Federal Reserve’s June dot plot showed nine of eighteen FOMC members projecting at least one rate hike in 2026 — a hawkish signal that had rattled equity markets and pressured growth assets. The weak jobs print fundamentally altered that calculus, raising the prospect that Chair Warsh’s second meeting on July 28-29 may see a meaningful moderation of the tightening language. Whether the Fed interprets one soft labor market reading as sufficient justification to stand down from its inflation-fighting posture — in the context of a May CPI that ran at 4.2% annually — remains the central question heading into earnings season. Separately, the week marked the start of the third quarter; all QTD figures in this week’s data reflect only the first four trading days of Q3.

Domestic Equities

The broad equity market staged a meaningful recovery, with the S&P 500 gaining +1.73% for the week and the Dow advancing +1.91%. The rally was led by rate-sensitive and consumer-facing sectors that had been most punished by the prior FOMC meeting’s hawkish shift. Communication Services surged +4.39%, recovering a portion of the prior week’s -6.22% loss as the prospect of a less aggressive Fed reduced the discount rate applied to long-duration growth cash flows. Consumer Discretionary rose +4.36%, benefiting from the same dynamic alongside renewed optimism that a softening labor market may prompt the Fed to forgo further tightening and preserve consumer spending power. Health Care extended its powerful run, gaining another +5.34% — its second consecutive week of outsized gains — as the sector rotation from mega-cap technology continued and investors accumulated quality health care names at still-attractive valuations. Financials advanced +4.13% despite the implications of potential rate cuts; markets appeared to view the labor market slowdown as a manageable soft landing scenario rather than a credit-threatening contraction.

The NASDAQ 100 declined modestly at -0.37%, underperforming the broader market for a third consecutive week as Information Technology inched down -0.18% — still unable to find sustained footing after the Broadcom-triggered AI demand repricing in early June. The equal-weighted S&P 500 gained +1.54%, moving broadly in line with the cap-weighted index, suggesting that the recovery this week was somewhat more balanced than recent weeks’ dramatic divergences. Small-cap indices were mixed: the Russell Micro Cap rose +2.70%, but the Russell 2000 slipped -0.34%, with growth-oriented small caps (-1.11%) continuing to underperform their value counterparts (+0.51%).

International Equities

International developed markets had an excellent week, with the MSCI EAFE advancing +2.77% — its strongest performance in several weeks. Germany was the standout, with MSCI Germany surging +4.68%, as improving global trade sentiment and receding Strait of Hormuz energy-cost pressures offered a constructive backdrop for European industrial and export-oriented names. MSCI UK All Cap rose +2.83% and MSCI Japan gained +2.37%, with the latter supported by ongoing corporate reforms and easing yen pressure as the U.S. rate outlook softened. The broad MSCI World index gained +2.10% for the week and MSCI ACWI rose +1.97%.

Emerging markets also participated in the recovery, with MSCI EM rising +1.04%. MSCI China posted a notable +3.47% advance — a welcome change after weeks of persistent underperformance — as the combination of a weaker dollar, easing global rate pressures, and incremental domestic policy support offered some relief to Chinese equities. MSCI India Domestic was essentially flat at -0.09%, consolidating after several volatile weeks. Year-to-date, MSCI EM continues to lead all major global equity regions at +24.06%, anchored by the broad emerging market universe outside of China, where structural growth dynamics remain intact.

Fixed Income

Despite the week’s dramatically weak jobs report — which caused an immediate rally in Treasuries on Thursday — fixed income ended the week modestly in the red, as the early days of the shortened week saw yields drift higher on ongoing inflation concerns ahead of the data. The Bloomberg US Aggregate Bond Index fell -0.41% for the week and Bloomberg US Treasuries declined -0.40%, with the positive Thursday reaction insufficient to offset the earlier yield pressure. Bloomberg US Corporate Bond fell -0.42%, though credit spreads held relatively contained as the weak labor data was widely interpreted as reducing systemic risk rather than flagging credit deterioration. The Bloomberg Global Aggregate Float Adjusted Index declined -0.18%, as the dollar softened modestly on rate repricing.

The medium-term picture for fixed income is improving at the margin: the Bloomberg US Aggregate Bond remains up +0.48% year-to-date, and the combination of a cooling labor market and the Iran ceasefire’s disinflationary impact on energy prices creates a more constructive path for duration assets in the second half of 2026 than existed just one month ago. The July 28-29 FOMC meeting and June CPI data will be decisive in confirming or complicating this improving backdrop.

Alternatives & Commodities

Gold rebounded +1.93% for the week as the sharply weak jobs report reduced real yield expectations and softened the dollar, restoring some of the haven asset’s relative appeal. Despite the weekly bounce, gold remains -4.96% year-to-date, having surrendered all of its early-year gains during the June selloff driven by rising real yields and reduced geopolitical risk premium following the Iran ceasefire. The metal’s trajectory in the second half of 2026 will depend heavily on the inflation and rates path: a genuine disinflation trend — driven by falling energy prices as the Strait of Hormuz reopens — would likely keep real yields elevated and continue to weigh on gold, while any resurgence of geopolitical uncertainty or fiscal concerns could rekindle safe-haven demand.

Energy declined -1.36% for the week, as the gradual progress in Strait of Hormuz reopening continued to dampen crude prices, though the pace of physical restoration has been slower than initially anticipated. The FTSE NAREIT Composite gained +0.57%, a modest but positive result that reflects both the income-oriented appeal of real estate in a softening rate environment and ongoing position consolidation following its strong recent run. REITs are now up +16.00% year-to-date — one of the better-performing asset classes in 2026 — and stand to benefit meaningfully if the Fed’s tightening bias recedes in response to the labor market data.

Source: Morningstar. Market data as of July 2, 2026. Past performance is not indicative of future results. The information provided is for educational and informational purposes only and does not constitute investment advice.