Looking Ahead This Week: April 27, 2026

The week ahead brings what may be the most consequential policy meeting of the year. The Federal Reserve’s April 28–29 FOMC meeting, which could be Jerome Powell’s final as Chair, will offer the Committee’s first opportunity to assess the full arc of the Iran conflict’s economic impact—from the inflationary spike of March through the sharp reversal and now partial rebound in oil prices. The market is not pricing in a rate change, but the tone of the statement and press conference will shape expectations for the second half of the year. Q1 earnings season continues at full pace, with a large number of major companies reporting in the week ahead, and the momentum from an 80%-plus beat rate will be tested by results from some of the market’s most heavily weighted names.

The ceasefire’s durability remains the most important unresolved variable. Oil prices back above $105, declining German business sentiment, and the fragility evident in European equity markets all suggest that the geopolitical risk premium has not been fully extinguished. The technology sector’s extraordinary performance—Intel’s 24% gain, the semiconductor index’s 18-day winning streak, Nvidia at $5 trillion—reflects genuine fundamental strength in AI-driven capital expenditure, but also raises concentration risk questions as the gap between technology leadership and the average stock continues to widen. Portfolio construction across sectors, geographies, and asset classes remains as important as ever in what continues to be a market shaped by rapidly evolving macro and geopolitical forces.

Economic Data and Market Highlights: Week of April 20, 2026

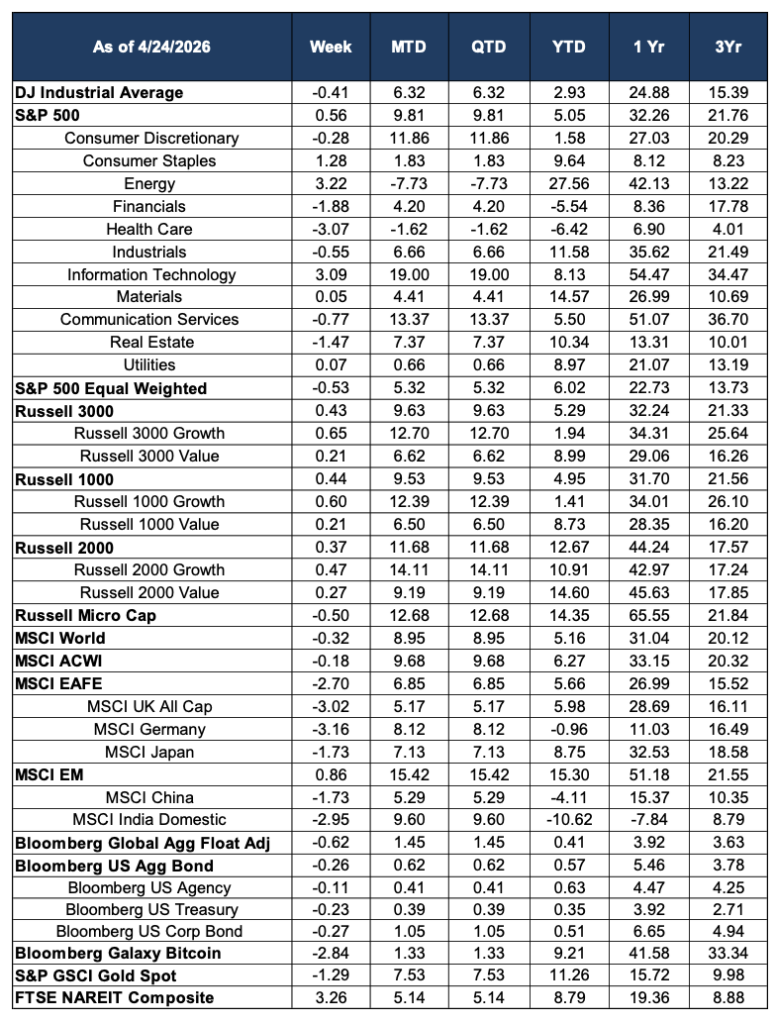

U.S. equity markets posted a modest but record-setting week ending April 24, 2026, as an extraordinary technology rally more than offset renewed geopolitical uncertainty and sector-specific weakness. The S&P 500 gained 0.56% on the week and closed at a new all-time high on Friday, while the Nasdaq Composite surged to its own record close, driven by one of the most dramatic single-stock earnings moves of the year. The Dow Jones Industrial Average slipped 0.41%, reflecting the market’s increasingly concentrated performance around the technology and semiconductor complex. With the S&P 500 now up 5.05% year-to-date, the full-circle recovery from a trough loss approaching 10% in mid-March represents a remarkable 15-point turnaround driven by geopolitical de-escalation, strong corporate earnings, and resurgent AI-driven capital investment.

The week’s defining event was Intel’s first-quarter earnings report, released after Thursday’s close, which sent shares surging 24% on Friday—the chipmaker’s best single-day gain since 1987. Intel posted earnings per share of $0.29 against estimates of just $0.02, with revenue of $13.58 billion exceeding the $12.41 billion consensus, as AI-driven business revenue grew 40% year-over-year. The report ignited the broader semiconductor complex: Advanced Micro Devices rallied nearly 14%, Qualcomm climbed more than 10%, and the Philadelphia Semiconductor Index extended its winning streak to 18 consecutive sessions, gaining roughly 40% since March 30. Nvidia reclaimed a $5 trillion market capitalization. A separate but market-positive development arrived when the Department of Justice announced it was dropping its investigation into Federal Reserve Chair Jerome Powell, removing a source of institutional uncertainty around Fed leadership and smoothing the path for Kevin Warsh’s expected succession.

Macro Backdrop: Ceasefire Fragility, Rising Oil, and the Fed on Deck

The geopolitical picture grew more complex this week as the Iran ceasefire showed renewed signs of strain. Brent crude futures climbed back above $105 per barrel as reports emerged of continued violations and uncertainty over the ceasefire’s extension beyond its initial two-week window. European markets bore the brunt of this renewed anxiety, with the pan-European Stoxx 600 declining multiple sessions as investors reassessed whether the energy risk premium—so decisively priced out just two weeks ago—might be returning. German business sentiment deteriorated sharply, with the Ifo Institute’s monthly business climate index falling to 84.4 in April, its lowest reading since the onset of the COVID-19 pandemic in May 2020, as German officials halved their 2026 GDP growth forecast to just 0.5%. The Energy sector’s weekly gain of 3.22% within U.S. equities is a direct reflection of this renewed oil price uncertainty.

Against this backdrop, the Federal Reserve meets April 28–29 in what may be Jerome Powell’s final rate decision as Chair. No policy change is expected—the benchmark rate will almost certainly remain at 3.50%–3.75%—but the statement and press conference will be parsed carefully for any signal of how the Committee interprets the rapidly evolving inflation picture. The energy-driven March CPI spike is now likely to reverse significantly in April given the oil price retreat of recent weeks, but the renewed uptick in crude toward $105 introduces fresh uncertainty. Q1 earnings season continued to provide a constructive fundamental backdrop, with more than a quarter of S&P 500 companies having reported and over 80% beating both earnings per share and revenue estimates, marking the sixth consecutive quarter of double-digit year-over-year earnings growth.

Domestic Equities

Sector performance this week was defined by sharp divergence. Information Technology led with a gain of 3.09%, powered almost entirely by the Intel earnings surge and the subsequent ripple effect across the semiconductor ecosystem. Energy rebounded 3.22% as oil prices edged higher on ceasefire uncertainty. Consumer Staples rose 1.28%, providing defensive ballast to a week that saw considerable volatility beneath the surface. Materials and Utilities were essentially flat.

Health Care was the week’s notable laggard, declining 3.07%, as the sector continued to grapple with structural headwinds from policy changes affecting Medicaid and Medicare Advantage programs. The sector is now down 6.42% year-to-date, among the weakest performers in the S&P 500. Financials fell 1.88%, Real Estate declined 1.47%, and Industrials slipped 0.55%. Communication Services gave back 0.77% and Consumer Discretionary edged lower by 0.28% despite the broader technology tailwind.

The week’s performance reinforced how much of the market’s gains have been concentrated in large-cap technology. The S&P 500 Equal Weighted index fell 0.53%—a meaningful 109-basis-point underperformance relative to the cap-weighted index—signaling that the average stock declined even as the headline index rose to records. Growth continued to lead value across all capitalization tiers, and small and mid-cap names held up reasonably well, with the Russell 2000 gaining 0.37% and now up 12.67% year-to-date, one of the stronger year-to-date performances across major domestic indices.

International Equities

International developed markets had a difficult week, driven primarily by renewed geopolitical anxiety and deteriorating European economic data. The MSCI EAFE fell 2.70%, with Germany declining 3.16%, the UK dropping 3.02%, and Japan retreating 1.73%. The sharp reversal in European equities reflects both the direct economic exposure to elevated energy costs—with Brent crude back above $105—and the deteriorating business sentiment captured in the German Ifo data. Despite the weekly setback, the MSCI EAFE remains up 5.66% year-to-date, a meaningful outperformance relative to global benchmarks over the full year.

Emerging markets were more resilient, with the MSCI EM gaining 0.86% on the week and extending its year-to-date lead to an impressive +15.30%, the best performance of any major equity region globally. MSCI China declined 1.73% and remains negative at -4.11% year-to-date, while India fell 2.95% as it continues to work through a challenging period; the MSCI India Domestic index remains down 10.62% for the year. The MSCI ACWI slipped a marginal 0.18%, and the MSCI World declined 0.32%, reflecting the drag from developed international markets against a modestly positive U.S. result.

Fixed Income

Fixed income markets experienced modest pressure this week as oil’s renewed rise raised questions about the near-term inflation trajectory heading into the Fed meeting. The Bloomberg U.S. Aggregate Bond Index fell 0.26% on the week, though it remains positive year-to-date at +0.57%. U.S. Treasuries declined 0.23% and corporate bonds gave back 0.27% as credit spreads widened slightly in response to the geopolitical uncertainty. The Bloomberg Global Aggregate Float Adjusted index fell 0.62%, reflecting both the dollar’s modest strength and the repricing of global rate expectations. Despite the weekly pullback, fixed income year-to-date returns across all major categories remain in positive territory, a meaningful improvement from the pressure seen earlier in the year.

Alternatives & Commodities

Gold pulled back 1.29% on the week as the combination of a modestly stronger dollar and some reduction in immediate safe-haven demand weighed on the metal, but it retains an 11.26% year-to-date gain and a one-year return of 15.72%, reflecting the depth and durability of the structural bid that has supported it throughout the year. Bitcoin declined 2.84% on the week but remains up 9.21% year-to-date, its recovery from a -23% trough earlier in the quarter one of the more striking rebounds of 2026. Real estate investment trusts were a bright spot, with the FTSE NAREIT Composite gaining 3.26% on the week and holding its year-to-date gain of +8.79%, benefiting from the improving growth and rate outlook.

Source: Morningstar. Market data as of April 24, 2026. Economic and news data sourced from CNBC, TheStreet, FactSet, BBN Times, and Ifo Institute. Past performance is not indicative of future results. This commentary is for informational purposes only and does not constitute investment advice.