Looking Ahead This Week: July 13, 2026

This week may be the most consequential of the third quarter, with two major catalysts arriving in rapid succession. On Tuesday, July 14, the Bureau of Labor Statistics releases the June Consumer Price Index — the inflation reading markets have been anticipating since the Iran ceasefire deal promised to sharply reduce energy prices. Consensus forecasts call for headline CPI to fall to approximately 3.9% year-over-year, down from 4.2% in May, driven by a nearly 10% monthly decline in gasoline prices as the Strait of Hormuz begins its slow reopening. Core CPI, which excludes food and energy, is expected to remain stickier at approximately 2.9% annually. A softer-than-expected core reading could be the catalyst for a meaningful shift in the Federal Reserve’s posture ahead of the July 28-29 FOMC meeting.

Q2 earnings season launches in earnest with the major money center banks reporting Tuesday through Wednesday: JPMorgan Chase, Wells Fargo, Citigroup, and BlackRock on July 14, followed by Bank of America, Goldman Sachs, and Morgan Stanley on July 15. Expectations are elevated — sector-wide Q2 earnings growth is projected at approximately +12.6% year-over-year — and net interest margin trends, consumer credit quality, and management commentary on the economic outlook will be closely parsed. The combination of CPI data and bank earnings this week has the potential to either validate the constructive Q3 setup that markets are pricing, or to introduce fresh volatility heading into the heart of earnings season.

Economic Data and Market Highlights: Week of July 7, 2026

Macro Backdrop

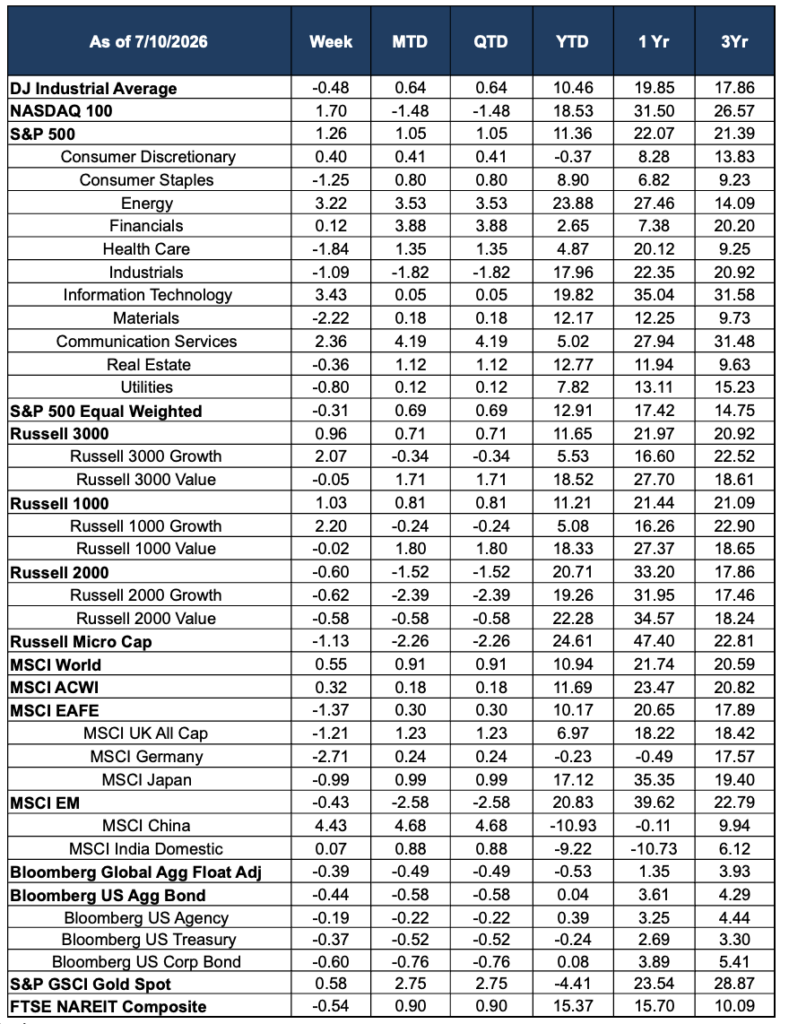

Markets entered the second week of Q3 in a positioning mode, with investors rotating back into large-cap technology and growth names ahead of what promises to be a pivotal stretch of macro data and earnings catalysts. The S&P 500 gained +1.26% for the week, extending its year-to-date return to +11.36%, but the headline masked a sharp divergence in market breadth: the equal-weighted S&P 500 fell -0.31%, confirming that the week’s gains were concentrated almost entirely in a handful of the largest technology and growth names. The NASDAQ 100 rose +1.70%, while the Dow Jones Industrial Average declined -0.48%, underscoring the sectoral nature of the rally.

The week’s primary macro focus was anticipatory rather than reactive: the June CPI report — not yet released as of this writing — is broadly expected to show a meaningful headline deceleration driven by the Iran ceasefire’s impact on gasoline prices. U.S. pump prices fell approximately 10% in June, the fourth-largest monthly decline in a decade, creating a significant mechanical tailwind for the headline inflation figure. If core inflation also shows incremental cooling, the Federal Reserve may find it increasingly difficult to maintain the tightening bias articulated in the June dot plot. The July 28-29 FOMC meeting is now the next major policy waypoint, and the week’s CPI and bank earnings data will heavily influence Warsh’s communication.

Domestic Equities

Technology staged its strongest rebound in weeks, with Information Technology gaining +3.43% — the sector’s best weekly performance since the post-Iran deal surge in mid-June. The move appeared driven by a combination of short-covering after the sector’s bruising multi-week selloff, anticipatory positioning ahead of Q2 earnings season, and growing confidence that the AI infrastructure spending cycle, while not without near-term noise, remains structurally intact. Communication Services also recovered +2.36%, adding to the prior week’s rebound in platform technology names. The Russell 1000 Growth index gained +2.20%, reversing the recent pattern of growth underperformance relative to value.

Energy was a notable positive surprise, rising +3.22% as the physical reopening of the Strait of Hormuz proved considerably more complex and time-consuming than markets had initially priced. With de-mining operations, vessel inspections, and insurance market normalization all still underway, crude oil prices partially recovered from their ceasefire-driven lows, providing a tailwind for the sector. Health Care gave back some of its recent outsized gains, declining -1.84%, as profit-taking set in after two exceptional consecutive weeks. Materials (-2.22%), Industrials (-1.09%), Consumer Staples (-1.25%), and Utilities (-0.80%) all declined, as the risk-on rotation toward growth and tech drew capital away from defensive and cyclical names. Small-cap indices underperformed, with the Russell 2000 falling -0.60% and Russell Micro Cap declining -1.13%, reinforcing the week’s theme of concentrated large-cap leadership.

International Equities

International developed markets retreated, with MSCI EAFE falling -1.37% for the week. MSCI Germany was the standout laggard, declining -2.71%, as softer eurozone growth data and concerns about the pace of the Strait of Hormuz reopening — which remains critical to European energy import normalization — weighed on sentiment. MSCI UK All Cap fell -1.21%, and MSCI Japan declined -0.99%, with the yen’s modest strengthening providing a headwind for Japanese exporters. The MSCI World index managed a modest +0.55% gain, buoyed by U.S. strength, while MSCI ACWI edged up just +0.32%.

Emerging markets were mixed, with the MSCI EM index declining -0.43% overall but with a striking divergence beneath the surface. MSCI China surged +4.43% — its strongest week in months — as incremental domestic policy support measures and signs of stabilization in the property sector drew renewed investor interest. With MSCI China now up +4.68% month-to-date after weeks of persistent selling, the question is whether this represents a genuine turning point or a tactical bounce in a structurally challenged market. MSCI India Domestic was essentially flat at +0.07%, while the broader EM region’s year-to-date return of +20.83% continues to reflect strength concentrated outside of China.

Fixed Income

Fixed income markets gave back ground for a second consecutive week, with the Bloomberg US Aggregate Bond Index falling -0.44% as Treasury yields drifted modestly higher on improving risk appetite and pre-CPI positioning. Bloomberg US Treasuries declined -0.37% and Bloomberg US Corporate Bond fell -0.60%, the latter reflecting a modest widening of credit spreads as Q2 earnings season approaches and uncertainty around credit quality trends increases. The Bloomberg Global Aggregate Float Adjusted Index fell -0.39%, as dollar firmness weighed on international bond returns.

The medium-term case for fixed income recovery remains intact but dependent on upcoming data. The Bloomberg US Aggregate Bond is now essentially flat for the year at +0.04%, and the June CPI report this week has the potential to be genuinely constructive for the asset class if headline deceleration is accompanied by any softening in core measures. A benign CPI reading, combined with the July 28-29 FOMC meeting, could set the stage for the first meaningful positive return period for core fixed income since early 2026.

Alternatives & Commodities

Gold posted a modest gain of +0.58% for the week, stabilizing after its prolonged June decline but still unable to decisively recover its lost 2026 gains. The metal sits -4.41% year-to-date, having surrendered its early-year advance as real yields rose on the Fed’s hawkish pivot and geopolitical risk premium contracted following the Iran ceasefire. The upcoming June CPI report is relevant for gold: a meaningful deceleration in headline inflation, driven by lower energy prices, may support the narrative that real yields could soon ease and allow gold to find firmer footing.

Energy’s +3.22% weekly advance was one of the week’s more telling market signals. The Strait of Hormuz reopening, while agreed upon diplomatically, is proceeding at a fraction of the pace that oil markets initially priced in. Technical challenges in restoring full tanker traffic — including the need for international mine-clearing operations and the restoration of insurer confidence — mean that the supply normalization process will be measured in months, not weeks. This dynamic provides a floor under oil prices and the Energy sector even as the geopolitical premium has largely unwound. Real estate investment trusts (FTSE NAREIT Composite) fell modestly at -0.54%, reflecting the week’s uptick in Treasury yields, though REITs remain up +15.37% year-to-date.

Source: Morningstar. Market data as of July 10, 2026. Past performance is not indicative of future results. The information provided is for educational and informational purposes only and does not constitute investment advice.