Looking Ahead This Week: June 22, 2026

Markets enter the week of June 22 navigating the simultaneous impacts of two historic events: a signed U.S.-Iran ceasefire memorandum of understanding and a hawkish pivot from the Federal Reserve’s updated dot plot. The operational reopening of the Strait of Hormuz is a process that experts estimate will take weeks to months, as de-mining, vessel inspections, and insurance market normalization must precede meaningful increases in tanker traffic. Energy markets will remain volatile as the market weighs the gap between the diplomatic reality and the physical reality of restored supply. Early movement in shipping rates and crude futures will be closely watched.

On the monetary policy front, the June dot plot’s hawkish shift — with nine of 18 FOMC members now projecting at least one rate hike in 2026 — will continue to reverberate through rate-sensitive assets. May PCE inflation data, due this week, will either validate or challenge the Fed’s tightening bias; a print below expectations could ease rate-hike fears and provide a relief rally for duration assets. Fed speakers will likely elaborate on the conditions necessary to trigger a hike versus an extended hold. The technology sector’s resilience in the face of a hawkish Fed and Iran deal-driven sector rotation will also be a key test of whether AI infrastructure spending momentum can maintain its grip on market leadership heading into the second half of 2026.

Economic Data and Market Highlights: Week of June 15, 2026

Macro Backdrop

The week of June 15 will be remembered as one of the most consequential in 2026, defined by two seismic developments that arrived in rapid succession and reshaped the macro landscape simultaneously. On June 14-15, President Trump and Iranian President Masoud Pezeshkian signed a memorandum of understanding to extend the ceasefire and commit to reopening the Strait of Hormuz — the strategic chokepoint through which approximately one-fifth of global oil and liquefied natural gas passes. The deal, while establishing only a 60-day framework for further negotiations, represented the most tangible progress toward normalizing energy supply since the conflict began in early 2026. Global markets surged on the news, with energy prices tumbling sharply and emerging market equities posting their strongest single-week gains of the year.

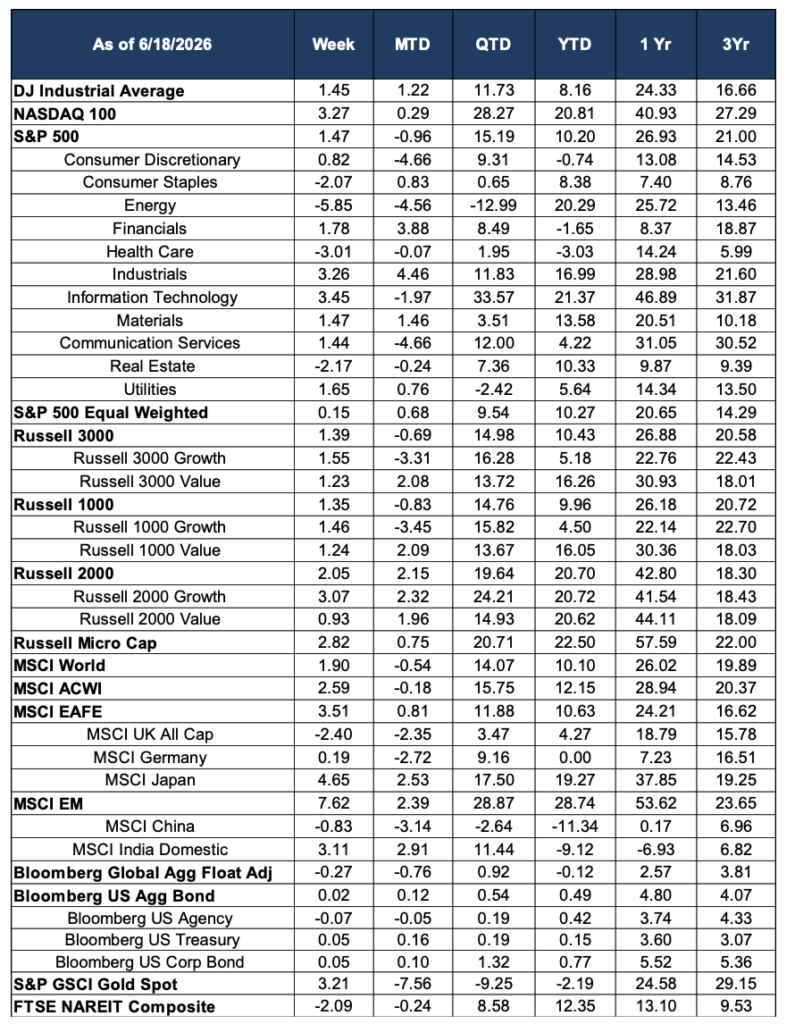

Just two days later, the Federal Reserve delivered its own landmark moment: Chair Kevin Warsh’s first FOMC rate decision kept the federal funds rate unchanged at 3.50–3.75%, but the accompanying Summary of Economic Projections marked a decisive policy shift. The updated dot plot showed the median FOMC member now projecting the federal funds rate ending 2026 at 3.8% — a full quarter-point above the current range — with nine of eighteen members penciling in at least one hike before year-end. Warsh notably did not submit his own dot, citing his long-held skepticism of forward guidance. The hawkish shift triggered an immediate market reaction: the S&P 500 fell -1.21% and Treasury yields jumped more than 16 basis points on Wednesday. However, the broader bullish macro narrative of the Iran deal proved sufficient to offset the FOMC shock by week’s end, with the S&P 500 ultimately closing up +1.47% for the week.

Domestic Equities

Despite the mid-week FOMC-driven turbulence, the S&P 500 advanced +1.47% for the week and the NASDAQ 100 surged +3.27%, as technology and growth stocks recovered sharply once markets absorbed the full implications of the Iran deal’s disinflationary tailwind. If energy inflation — which has been the primary driver of elevated CPI readings — begins to normalize as Strait of Hormuz shipping resumes, the case for Fed rate hikes weakens considerably. Information Technology gained +3.45%, its second consecutive week of solid gains following the Broadcom-triggered selloff in early June. Communication Services also recovered, adding +1.44%. Industrials were a notable standout at +3.26%, as a reopened global shipping corridor promises to reduce supply chain costs and support industrial demand.

Energy was the week’s clear laggard, tumbling -5.85% as oil prices fell sharply on the Strait of Hormuz deal. The sector has now declined -12.99% quarter-to-date, though its year-to-date return of +20.29% still leads most other areas of the market. Health Care fell -3.01%, suffering from both the hawkish FOMC rate implications for capital-intensive healthcare companies and a rotation away from defensives that had rallied during the geopolitical risk period. Real Estate declined -2.17% as the FOMC’s hawkish dot plot pushed yields higher and dampened appetite for rate-sensitive real assets. Consumer Staples fell -2.07% for similar reasons. The equal-weighted S&P 500 gained just +0.15%, reflecting how concentrated the week’s gains were in technology and the largest growth names — a partial reversal of the prior week’s broad-based rally.

International Equities

International markets were the standout performers of the week, as the Iran ceasefire deal carried particularly powerful implications for energy-importing economies. The MSCI EAFE surged +3.51%, its strongest weekly gain in months, driven by a remarkable +4.65% advance from MSCI Japan — where import-cost relief from lower oil prices is expected to meaningfully improve corporate margins and consumer purchasing power. MSCI UK All Cap was the notable exception, declining -2.40%, partly reflecting energy sector concentration within UK equity indices and some local election-related uncertainty.

Emerging markets were the week’s most dramatic beneficiary, with the MSCI EM index posting a stunning +7.62% gain — one of the strongest single-week performances for the asset class in years. The gains were particularly acute for energy-importing emerging economies, which had been disproportionately hurt by the Strait of Hormuz closure’s impact on both their trade balances and currency values. MSCI India Domestic surged +3.11%, reversing a multi-week decline. MSCI China was a notable laggard even within this powerful EM rally, falling -0.83%, as domestic economic headwinds continue to insulate Chinese equities from the broader geopolitical tailwind. Year-to-date, MSCI EM now leads all major global regions at +28.74%.

Fixed Income

Fixed income markets were caught in a tug-of-war between the Iran deal’s disinflationary implications and the FOMC’s hawkish dot plot pivot, ultimately ending the week essentially flat. The Bloomberg US Aggregate Bond Index gained just +0.02%, and Bloomberg US Treasuries edged up +0.05%, as the two forces very nearly offset each other. Bloomberg US Corporate Bond was also +0.05%, while the Bloomberg Global Aggregate Float Adjusted Index declined -0.27%, reflecting the stronger U.S. dollar’s impact on international bond returns.

The week crystallized the central tension facing fixed income investors for the second half of 2026: a Fed that has formally adopted a tightening bias argues for caution on duration, while a structural easing of the energy supply shock — if the ceasefire holds — argues for a meaningful reduction in forward inflation expectations. The resolution of this tension in the coming weeks and months will largely determine whether core fixed income can deliver meaningful positive returns in 2026. For now, the Bloomberg US Aggregate Bond sits at +0.49% year-to-date, and investors are closely watching each data point for clues about where this tug-of-war resolves.

Alternatives & Commodities

Gold rebounded +3.21% for the week, partially recovering from its sharp June decline, as some safe-haven demand returned following the FOMC’s hawkish surprise and residual uncertainty about whether the Iran ceasefire will hold. Despite the weekly bounce, gold remains -2.19% year-to-date, a dramatic reversal from its April highs when it was one of the best-performing assets in the portfolio. The metal’s near-term trajectory will be heavily influenced by the inflation data path: if the Iran deal ultimately drives energy prices meaningfully lower and core PCE decelerates toward 3%, the case for gold as an inflation hedge diminishes even as geopolitical risk premium is repriced lower.

The Energy sector’s -5.85% weekly decline reflects markets pricing in the eventual return of approximately 20 million barrels per day of oil and LNG that had been blocked by the Strait of Hormuz closure. While the physical reopening of the strait will take time — experts estimate weeks to months for full restoration of traffic — the directional pricing shift was immediate and significant. FTSE NAREIT Composite declined -2.09% on the week as the hawkish FOMC outcome weighed on yield-sensitive real assets, though REITs retain a solid +12.35% year-to-date return. If the ceasefire holds and energy inflation subsides, the Fed’s tightening bias may ultimately prove short-lived, which would provide a constructive setup for rate-sensitive alternatives heading into the second half of the year.

Source: Morningstar. Market data as of June 18, 2026. Past performance is not indicative of future results. The information provided is for educational and informational purposes only and does not constitute investment advice.