Looking Ahead This Week: June 1, 2026

Markets enter June with momentum at their backs — nine straight weekly gains for the S&P 500, a record-high Dow, and a Nasdaq that posted its best monthly performance of 2026 in May — but several critical macro catalysts will test that resilience in the days ahead. The May nonfarm payrolls report, due Friday, will be closely watched for signs of labor market cooling that might give the Federal Reserve room to hold its current policy stance comfortably. With core PCE running at 3.3% annually and the Fed holding rates at 3.50–3.75%, any upside surprise in wages or job creation could reignite rate-hike speculation.

The geopolitical backdrop remains the most consequential wildcard. The U.S. and Iran have reportedly agreed on the terms of a 60-day ceasefire memorandum of understanding, though the deal still requires final approval from President Trump, and sporadic hostilities — including Iranian missile activity late in the week — underscore the fragility of the arrangement. A formal ceasefire and Strait of Hormuz reopening could drive another leg lower in energy prices, meaningfully reducing headline inflation and reshaping the Fed’s calculus. ISM manufacturing data and additional Fed speakers round out a data-heavy calendar. After nine weeks of gains, the market’s ability to absorb bad news will be tested.

Economic Data and Market Highlights: Week of May 25, 2026

Macro Backdrop

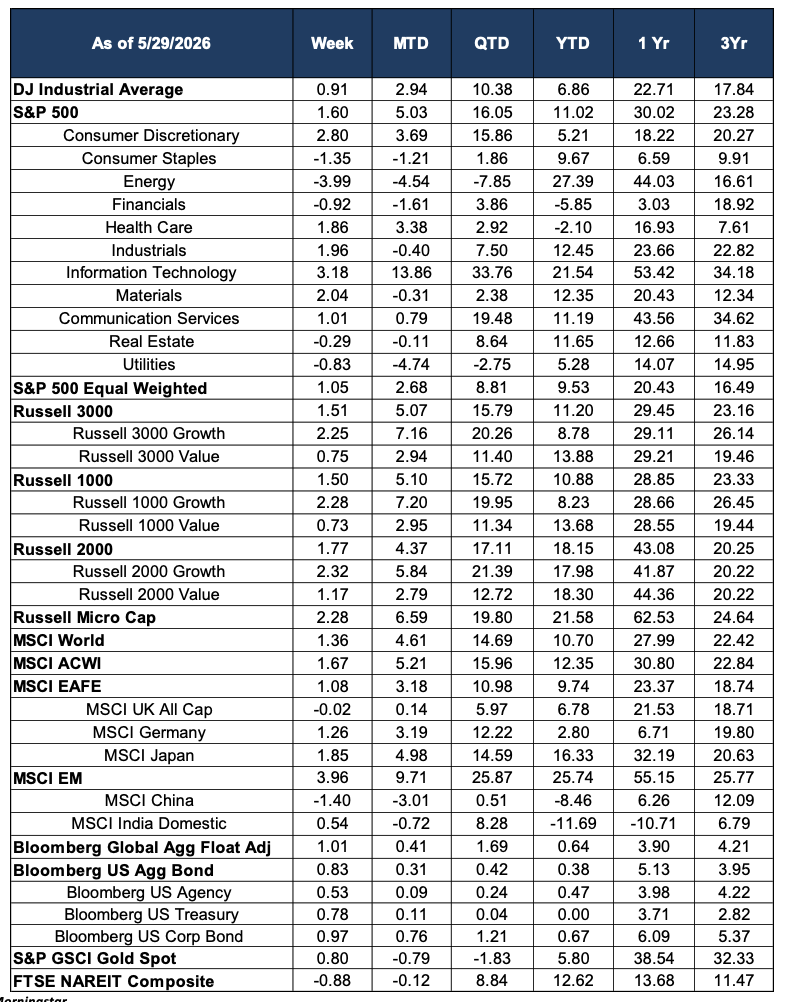

In a holiday-shortened week following Memorial Day, equities pushed higher for a ninth consecutive week — the S&P 500’s longest winning streak in over two years. The index gained +1.60% and closed May up approximately 5%, while the Dow crossed the 51,000 threshold for the first time in history, closing at 51,032 on Friday, May 29. The Nasdaq surged approximately 8% for the month of May, its best monthly performance of 2026. The dual engines of the week’s advance were AI-driven earnings momentum and continued optimism around U.S.-Iran ceasefire negotiations, which drove a dramatic unwinding of the energy price premium that had been embedded in markets since the Strait of Hormuz closure in late April.

April PCE inflation data, released May 28, came in largely in-line with expectations: core PCE rose 0.2% for the month and 3.3% annually, a modest deceleration from March and somewhat less alarming than the 3.8% headline CPI print reported the prior week. While inflation remains well above the Federal Reserve’s 2% target, the in-line reading provided markets some reassurance that the disinflation trend has not reversed entirely. The Fed held rates steady at its April 28-29 meeting, though a majority of officials indicated that further tightening could become appropriate if inflation persists. Markets continue to price virtually no chance of rate cuts through 2026, with rate-hike odds remaining elevated heading into summer.

Domestic Equities

Information Technology led all sectors for the week, gaining +3.18%, as Dell Technologies delivered one of the most stunning earnings reports in recent memory. Dell reported first-quarter revenue of $43.8 billion, up 88% year-over-year, with AI server revenue alone surging 757% from a year earlier to $16.1 billion. The company raised its full-year revenue outlook to approximately $167 billion and guided for $60 billion in AI server sales — well above prior estimates. Dell shares rose 32% on May 29 in the best single-day performance in the company’s history, amplifying AI infrastructure enthusiasm across the sector. The IT sector’s year-to-date gain now stands at +21.54%, reflecting the extraordinary capital deployment cycle underway in artificial intelligence.

Consumer Discretionary rebounded +2.80%, Industrials gained +1.96%, and Materials rose +2.04%, as the improving geopolitical outlook and softer PCE data supported broad risk appetite. Health Care added +1.86% and Communication Services rose +1.01%, rounding out a positive week for most of the market. The equal-weighted S&P 500 gained +1.05%, with leadership rotating across sectors in a constructive sign of market breadth. Energy was the clear laggard, falling -3.99% as crude prices tumbled — Brent crude posted its worst monthly performance since the COVID-19 pandemic in May, declining nearly 19% from its April highs as Iran ceasefire optimism took hold. Consumer Staples (-1.35%) and Utilities (-0.83%) also declined modestly as the risk-on tone reduced demand for defensive positioning.

International Equities

International markets participated meaningfully in the week’s advance. The MSCI EAFE gained +1.08%, with MSCI Japan leading developed market peers at +1.85% as ongoing corporate governance progress and yen dynamics continued to support Japanese equities. MSCI Germany rose +1.26%, though European markets broadly underperformed relative to the U.S. and emerging market benchmarks. MSCI UK All Cap was essentially flat at -0.02%, reflecting some caution around energy sector exposure given the sharp pullback in crude.

Emerging markets were a standout, with the MSCI EM index surging +3.96% for the week — one of its strongest single-week performances of the year. The MSCI EM benchmark now leads all major regions year-to-date at +25.74%, extending a remarkable run driven by dollar weakness, commodity dynamics, and improving risk appetite. MSCI China declined -1.40% for the week and remains down -8.46% year-to-date, continuing to diverge meaningfully from broader EM performance amid persistent domestic headwinds. MSCI India Domestic posted a modest +0.54% on the week, consolidating after sharp swings driven by energy import cost volatility.

Fixed Income

The bond market had its best week in several months, as Iran ceasefire optimism and the in-line PCE reading allowed Treasury yields to pull back from their recent highs. The Bloomberg US Aggregate Bond Index gained +0.83%, and Bloomberg US Treasuries rose +0.78%, as rate-hike fears moderated. Bloomberg US Corporate Bond returned a strong +0.97% for the week, supported by tightening credit spreads as the macro outlook improved on the margin. The Bloomberg Global Aggregate Float Adjusted Index also turned in a solid +1.01% weekly performance.

The cumulative picture for fixed income in 2026 reflects the challenging rate environment: the Bloomberg US Aggregate is up only +0.38% year-to-date, while Treasuries are essentially flat (0.00% YTD). The week’s rally is a reminder of how quickly bond market dynamics can shift when the inflation and geopolitical narratives evolve — a potential ceasefire and lower energy prices could meaningfully reduce the pressure on the Fed’s policy path and extend the recovery in fixed income.

Alternatives & Commodities

Gold recovered modestly, gaining +0.80% for the week, as the in-line PCE data and ongoing geopolitical uncertainty maintained some safe-haven demand. Year-to-date, gold remains up +5.80% and has delivered +38.54% over the trailing twelve months, reflecting its effectiveness as a portfolio diversifier through 2026’s volatile macro environment. The commodity complex broadly reflected the Iran ceasefire narrative: Energy prices continued to fall sharply, with Brent crude having now declined approximately 20% from its 2026 highs, dragging the Energy sector’s weekly return to -3.99%. Despite the recent retreat, Energy remains the top-performing S&P 500 sector year-to-date at +27.39%, a testament to the extraordinary supply shock that dominated the first half of 2026.

Real estate investment trusts (FTSE NAREIT Composite) slipped -0.88% for the week despite the positive yield backdrop, suggesting some profit-taking after the sector’s strong prior-week performance. The REIT sector remains up +12.62% year-to-date, and the improving yield environment — if sustained by a formal ceasefire and easing energy inflation — could provide a constructive setup for rate-sensitive real assets heading into the second half of the year.

Source: Morningstar. Market data as of May 29, 2026. Past performance is not indicative of future results. The information provided is for educational and informational purposes only and does not constitute investment advice.