Looking Ahead This Week: May 25, 2026

Markets enter a holiday-shortened week — U.S. exchanges are closed Monday, May 25 for Memorial Day — with investors closely monitoring the evolving U.S.-Iran diplomatic negotiations. Progress toward a ceasefire deal and the reopening of the Strait of Hormuz could send oil prices meaningfully lower, shifting the sectoral leadership that has defined much of 2026. Conflicting signals from both sides late in the prior week underscore that a final agreement remains fluid, and any breakdown in talks could quickly reverse oil’s retreat.

On the data front, the April Personal Consumption Expenditures (PCE) price index — the Federal Reserve’s preferred inflation gauge — is due later in the week, and investors will be watching closely after April CPI printed at a three-year high of 3.8%. Fed officials are expected to continue striking a cautious tone, with rate cut expectations essentially eliminated through 2027. Second-quarter earnings season winds down with a handful of major retailers and industrials reporting. With the S&P 500 logging its eighth consecutive weekly gain, stretched valuations and persistent macro headwinds keep the risk-reward calculus delicate heading into the summer months.

Economic Data and Market Highlights: Week of May 18, 2026

Macro Backdrop

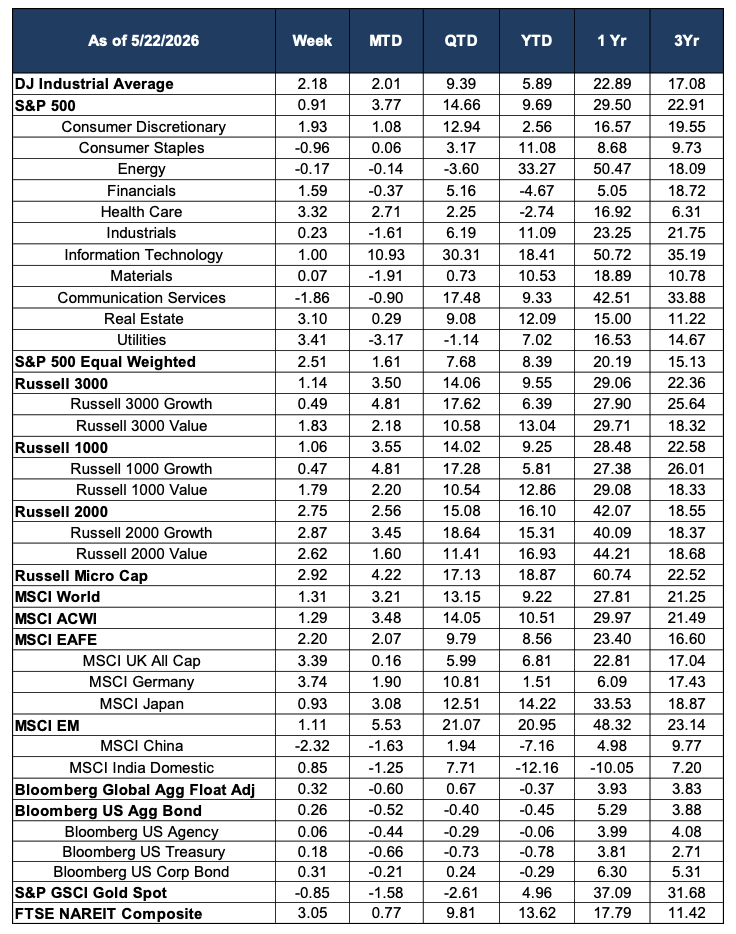

Equity markets posted their eighth consecutive week of gains — the longest such winning streak since late 2023 — as a combination of moderating Treasury yields, progress in U.S.-Iran diplomatic talks, and resilient corporate earnings underpinned investor confidence. The Dow Jones Industrial Average rose +2.18% and set a new intraday record high on May 22, closing above 50,579, while the S&P 500 advanced +0.91% to finish near 7,473. Breadth improved notably from the prior week: the equal-weighted S&P 500 gained +2.51%, and small-cap benchmarks led the way higher, suggesting the rally broadened beyond mega-cap technology names.

The week’s most closely watched event was Nvidia’s earnings report on May 20, which delivered record first-quarter revenue of $81.6 billion — an 85% year-over-year increase — and earnings per share of $1.87 versus analyst estimates of $1.76. Despite the blowout results, shares fell approximately 1.5% in after-hours trading and remained under modest pressure through the week, a textbook ‘sell the news’ response after the stock had rallied materially into the report. Nvidia’s forward guidance for $91 billion in fiscal second-quarter revenue was well above consensus, reinforcing the structural strength of AI infrastructure demand even as near-term valuation scrutiny intensified. Separately, Iran-U.S. peace talks gained traction late in the week, with both sides signaling diplomatic progress, which contributed to a modest easing of Treasury yields and drove meaningful weakness in energy prices.

Domestic Equities

The week’s rally was notably broad-based, with value and cyclical sectors reclaiming leadership. Utilities surged +3.41% as Treasury yields pulled back from their recent highs, restoring relative appeal to dividend-paying defensive names. Health Care gained +3.32% and Real Estate rose +3.10%, both benefiting from the same rate-relief dynamic and representing a sharp reversal from their underperformance in the prior inflation-shock week. Consumer Discretionary rebounded +1.93%, aided by modest stabilization in consumer sentiment data.

Information Technology advanced +1.00%, a somewhat restrained result given Nvidia’s record revenue print, as the sell-the-news reaction in NVDA weighed on sentiment across the semiconductor and AI hardware complex. Communication Services was the lone notable laggard, falling -1.86%, pressured by weakness in select advertising and streaming names. Energy essentially flatlined at -0.17% as Iran peace talk optimism capped crude prices. Small-cap stocks were a standout performer: the Russell 2000 gained +2.75% and the Russell Micro Cap index rose +2.92%, reflecting improved risk appetite and a rotation toward areas of the market that had lagged during the concentrated large-cap rally of recent months.

International Equities

International developed markets had a strong week, with the MSCI EAFE advancing +2.20%. European markets led the gains: MSCI Germany rose +3.74% and MSCI UK All Cap climbed +3.39%, supported by easing energy import cost pressures as oil retreated on Iran ceasefire optimism, and by improved risk appetite broadly. MSCI Japan posted a more modest +0.93%, consolidating recent gains as the yen strengthened slightly, creating a modest headwind for export-oriented names. Year-to-date, Japan remains a strong performer at +14.22%.

Emerging markets were also positive on balance, with the MSCI EM index gaining +1.11% for the week and extending its year-to-date lead to +20.95%, maintaining its position as the top-performing major region globally. MSCI India Domestic recovered +0.85% after its sharp decline the prior week. China continues to be an outlier to the downside within emerging markets, with MSCI China falling -2.32% on the week and -7.16% year-to-date, as persistent domestic headwinds and geopolitical concerns continue to weigh on Chinese equity valuations.

Fixed Income

Fixed income markets found modest relief as Treasury yields retreated from the prior week’s inflation-driven spike. The Bloomberg US Aggregate Bond Index gained +0.26%, and Bloomberg US Treasury returned +0.18%, as the easing in rate-hike expectations — driven partly by Iran peace talk optimism reducing the energy price overhang — allowed yields to settle lower. Bloomberg US Corporate Bond returned +0.31%, with investment-grade credit continuing to demonstrate resilience amid a supportive corporate earnings backdrop.

Despite the weekly improvement, the medium-term picture for fixed income remains challenging. The Bloomberg US Aggregate Bond is down -0.45% year-to-date, and Treasuries are off -0.78% YTD, reflecting the cumulative pressure of a Federal Reserve that has been unable to cut rates in an environment of above-target inflation. With the April PCE report due in the coming days, fixed income allocators remain in a watchful posture, balancing near-term yield relief against a macro environment that offers limited conviction on the direction of rates.

Alternatives & Commodities

Gold pulled back a further -0.85% for the week, extending its modest retreat from recent highs, as easing geopolitical tensions — specifically the Iran-U.S. diplomatic progress — reduced immediate safe-haven demand. Still, gold remains up +4.96% year-to-date and +37.09% over the trailing twelve months, reflecting the meaningful role it has played as a portfolio diversifier through a volatile 2026. Energy prices declined as well, with the S&P GSCI Gold Spot down, and the Energy sector essentially flat at -0.17% for the week, as Brent crude slipped toward the low $100s on hopes of a Strait of Hormuz reopening. Crude oil fell approximately 6% on the week as peace talk headlines filtered through the market, though follow-through remains contingent on a formal agreement.

Real estate investment trusts (FTSE NAREIT Composite) were a bright spot this week, gaining +3.05%, as the easing in Treasury yields restored appetite for rate-sensitive real assets. The sector is now up +13.62% year-to-date, representing a meaningful recovery from its earlier 2026 lows. The performance of REITs, Utilities, and other yield-sensitive categories this week serves as a reminder that fixed income alternatives can move quickly when the rate narrative shifts — even modestly.

Source: Morningstar. Market data as of May 22, 2026. Past performance is not indicative of future results. The information provided is for educational and informational purposes only and does not constitute investment advice.