Looking Ahead This Week: May 11, 2026

The April Consumer Price Index report, due this week, is arguably the most anticipated economic release of the quarter. After March’s energy-driven headline spike to 3.3%, investors and policymakers are watching carefully to see how much of the subsequent oil price retreat has flowed through to consumer prices. With Energy sector stocks now down nearly 10% from their quarter-to-date peak, the directional shift in commodity markets should be reflected in the April data—but the degree of relief will determine whether the Federal Reserve, under incoming Chair Kevin Warsh, can credibly begin to signal a more accommodative stance for the second half of the year. Core CPI, which has been tracking at a relatively well-behaved 2.6%, is the figure that will attract the most scrutiny.

The other event commanding attention this week is the evolving ceasefire situation in the Middle East. The fragile truce between the United States, Israel, and Iran held through the prior week but with continued volatility—oil prices swung from above $114 to below $100 and back again as reports of skirmishes near the Strait of Hormuz alternated with reassurances from Washington that the agreement remained in place. Any definitive shift in the durability of the ceasefire—in either direction—will have immediate market consequences. Investors are also looking ahead to Nvidia’s fiscal first-quarter earnings, expected May 20, which will serve as the definitive capstone to one of the strongest technology earnings seasons in memory. Consensus estimates call for year-over-year EPS growth of approximately 118% and revenue growth of nearly 79%, reflecting the extraordinary scale of AI infrastructure investment currently underway.

Economic Data and Market Highlights: Week of May 4, 2026

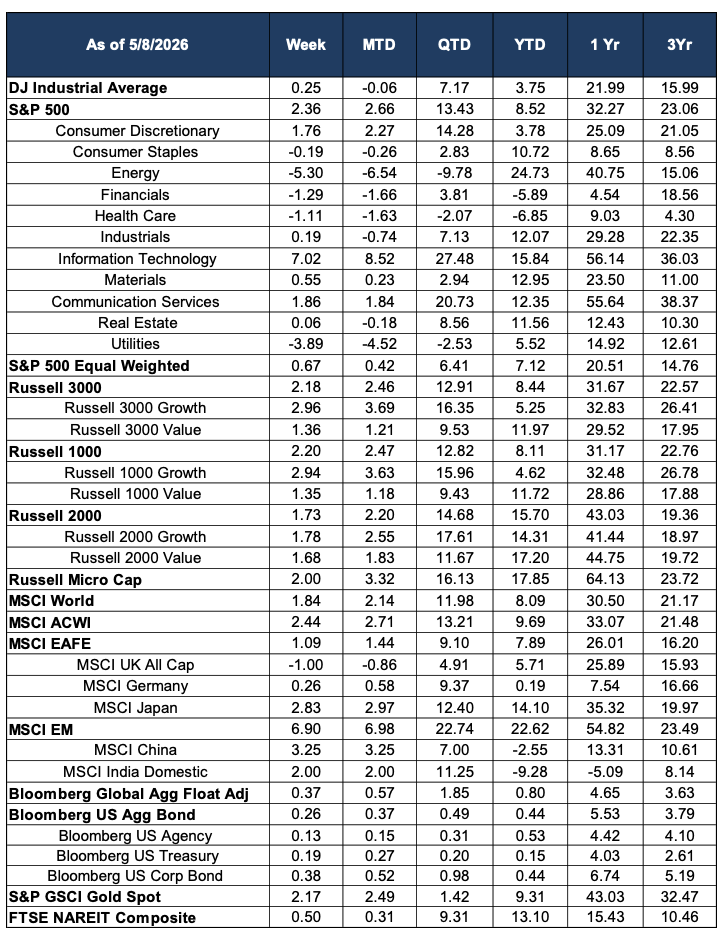

U.S. equity markets delivered their sixth consecutive week of gains ending May 8, 2026—the longest winning streak since 2024—as an extraordinary technology earnings season and a resilient labor market propelled the S&P 500 to yet another record close. The index gained 2.36% on the week, pushing its year-to-date return to +8.52% and closing near 7,399. The Nasdaq Composite surged 4.5% on the week, lifted by a wave of Magnificent Seven results that collectively validated the AI infrastructure investment thesis and reset expectations for full-year earnings growth. The Dow Jones Industrial Average posted a more modest advance of 0.25%, reflecting the week’s highly concentrated character: leadership was almost entirely driven by mega-cap technology, while most other areas of the market either tread water or pulled back.

The week’s macro backdrop included a supportive but nuanced April employment report. Nonfarm payrolls rose 115,000—above the 55,000 consensus forecast—marking the strongest back-to-back monthly gain since 2024. The unemployment rate held steady at 4.3%, and average hourly earnings rose a softer-than-expected 0.2% month-over-month and 3.6% year-over-year, providing reassurance that wage-driven inflation pressures remain contained. Federal government employment continued to decline, a trend that has been a feature of recent reports. The combination of above-consensus job creation and subdued wage growth is constructive for the Fed’s inflation calculus as Warsh prepares to take the helm.

Macro Backdrop: AI Earnings Validate the Cycle, Ceasefire Holds—Barely

The defining macro story of the week was the confirmation—delivered through the combined weight of Microsoft, Meta, Alphabet, and Amazon’s Q1 results—that AI capital expenditure is accelerating rather than plateauing. Microsoft beat earnings estimates with adjusted EPS of $4.27, Meta reported a stunning 61% year-over-year earnings increase to $10.44 per share, and Alphabet posted cloud revenue growth of 63%, with all four companies raising their full-year capital expenditure guidance. Combined, the six Magnificent Seven members that have reported are tracking toward approximately 45.7% year-over-year earnings growth. These results have effectively silenced near-term concerns about AI return on investment and reset the narrative around technology spending for the rest of 2026. Nvidia’s results, expected May 20, will serve as the final verdict.

The geopolitical backdrop remained volatile. The Iran ceasefire continued to hold in name, though skirmishes near the Strait of Hormuz triggered several intraday oil price spikes—including a single-session surge of nearly 6% that briefly pushed Brent above $114. The U.S. subsequently confirmed the ceasefire remained formally intact despite the exchanges, and oil prices retraced toward the mid-$100s. The sustained uncertainty is reflected in the Energy sector’s continued weakness, as investors weigh the probability of a permanent resolution against the possibility of renewed escalation. The IEA has characterized the Hormuz closure as the largest supply disruption in the history of the global oil market, and while markets appear to have partially discounted an extended disruption, any deterioration in the diplomatic track would quickly reprice that assumption.

Domestic Equities

Information Technology dominated all other sectors by a wide margin, gaining 7.02% on the week and extending its quarter-to-date return to an extraordinary +27.48%. The sector has become the primary engine of index returns in Q2, driven first by the semiconductor recovery and now amplified by the wave of AI-related earnings beats from the platform companies. Communication Services added 1.86% and Consumer Discretionary gained 1.76%, both sectors benefiting from mega-cap strength and positive consumer data. Materials rose 0.55%, Industrials edged up 0.19%, and Real Estate was essentially flat at +0.06%.

The week’s laggards reflected a decisive de-risking from the defensive and commodity-linked positions that had defined the prior two months. Energy fell 5.30%—its worst week in some time—continuing the reversal from a peak year-to-date gain exceeding 41%. Despite this week’s decline, the sector retains a 24.73% year-to-date gain, a testament to the magnitude of the war-driven move. Utilities fell 3.89%, as rising growth optimism and higher equity valuations reduced the appeal of defensive yield. Health Care declined 1.11%, extending its year-to-date loss to -6.85% as policy-driven structural headwinds persist. Financials slipped 1.29%.

The equal-weighted S&P 500 gained just 0.67%—a 169-basis-point gap versus the cap-weighted index—confirming that the week’s gains were highly concentrated in the largest technology names. Growth continued to meaningfully outpace value: Russell 1000 Growth returned 2.94% versus 1.35% for Russell 1000 Value. Small caps participated constructively, with the Russell 2000 rising 1.73% and now up a strong +15.70% year-to-date, while the Russell Micro Cap gained 2.00% and has extended its year-to-date advance to +17.85%, one of the standout performers in the domestic market.

International Equities

Emerging markets were the international story of the week, with the MSCI EM surging 6.90%—one of the strongest single-week gains in years—and extending its year-to-date return to a remarkable +22.62%, the best performance of any major equity region by a substantial margin. MSCI China gained 3.25% and MSCI India advanced 2.00%, as improving risk sentiment, a modestly weaker dollar, and the prospect of lower energy costs for oil-importing economies all contributed to the move. The year-to-date story for emerging markets has been one of the most compelling portfolio themes of 2026, particularly for investors who maintained geographic diversification through the difficult first quarter.

In developed international markets, Japan led with a gain of 2.83% on the week and a year-to-date return of +14.10%, one of the strongest among major developed markets globally. The MSCI EAFE advanced a more modest 1.09%, as weakness in the UK (-1.00%) and Germany (+0.26%) offset Japan’s strength. The MSCI ACWI gained 2.44% and the MSCI World rose 1.84%. Despite the weekly underperformance of European markets, the MSCI EAFE remains up 7.89% year-to-date, still ahead of the S&P 500’s 8.52% but the gap has narrowed considerably as U.S. technology leadership has reasserted itself.

Fixed Income

Fixed income markets were broadly positive on the week, as soft wage data and a moderated inflation outlook supported bonds alongside the equity rally. The Bloomberg U.S. Aggregate Bond Index gained 0.26%, pushing its year-to-date return to +0.44%. Corporate bonds led with a gain of 0.38% as credit spreads tightened in the improving growth environment. U.S. Treasuries gained 0.19% and Agency debt added 0.13%. The Bloomberg Global Aggregate Float Adjusted index advanced 0.37% and is now up 0.80% year-to-date. The constructive simultaneous performance of equities and fixed income reflects a market increasingly pricing a soft-landing scenario, supported by resilient employment, moderating wages, and an earnings season that has exceeded virtually every expectation.

Alternatives & Commodities

Gold continued to build on its year-to-date performance, gaining 2.17% on the week and extending its advance to +9.31% for the year, with a one-year return of +43.03%. The metal’s continued strength alongside a broad equity rally reinforces the view that structural demand—central bank accumulation, long-term inflation hedging, and geopolitical risk premium—is sustaining this cycle’s gold bull market independent of short-term risk sentiment shifts. Real estate investment trusts were constructive, with the FTSE NAREIT Composite gaining 0.50% and now up +13.10% year-to-date, continuing to benefit from the improving economic outlook and the expectation that the rate cycle’s next move will eventually be downward.

Source: Morningstar. Market data as of May 8, 2026. Economic and news data sourced from CNBC, Bloomberg, FactSet, BLS, Al Jazeera, Fortune, and TheStreet. Past performance is not indicative of future results. This commentary is for informational purposes only and does not constitute investment advice.