Economic Data and Market Highlights

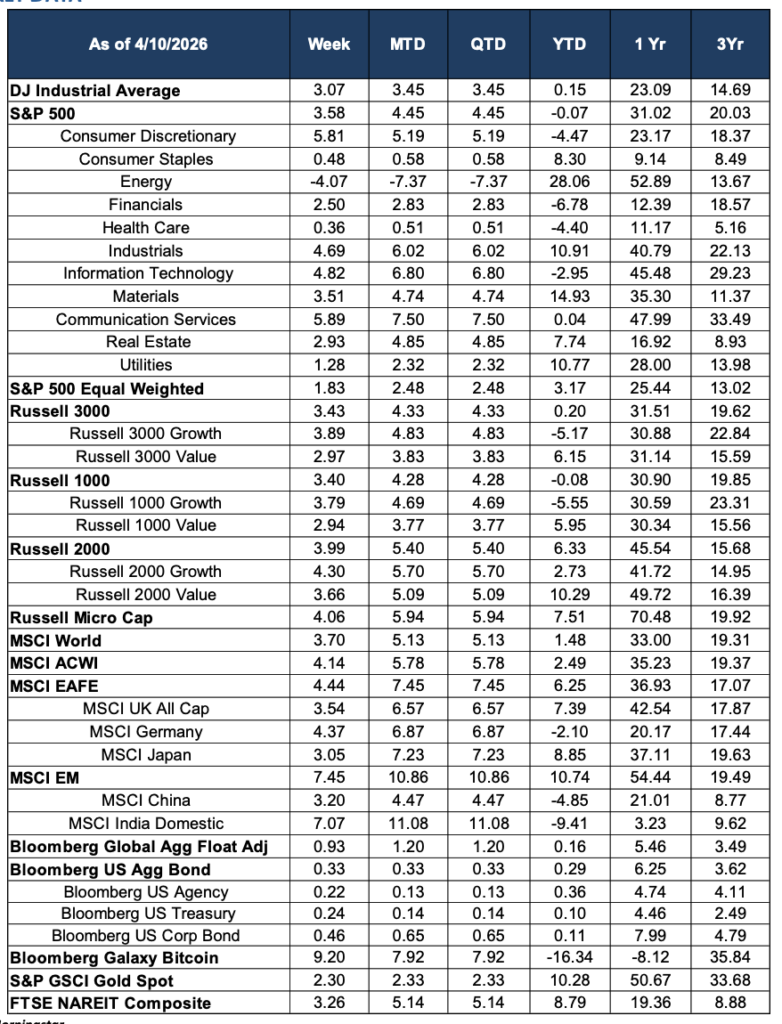

Global equity markets surged during the week ending April 10, 2026, posting their best weekly performance since November as a Pakistan-brokered ceasefire between the United States and Iran ignited one of the most powerful single-day rallies of the year. The S&P 500 gained 3.58% on the week, bringing its year-to-date return to essentially flat at -0.07%—a remarkable recovery from a trough that had the index down nearly 10% from its January peak. The Dow Jones Industrial Average advanced 3.07%, pushing its year-to-date return into positive territory at +0.15% for the first time since early in the year. For the second consecutive week, equity markets demonstrated the resilience of risk appetite when the principal macro headwind—the Middle East conflict and its energy price consequences—shows credible signs of abating.

The catalyst arrived on Tuesday, April 7, when President Trump’s administration, with Pakistan serving as a key diplomatic intermediary, announced a two-week “cooling-off” ceasefire. Under the terms of the agreement, the United States and Israel agreed to halt military strikes on Iran, while Tehran agreed to the complete reopening of the Strait of Hormuz. The announcement was met with an immediate and forceful market response: the Dow Jones jumped more than 1,300 points in a single session, its best day since April 2025, while WTI crude futures plunged more than 16% in their largest single-day decline since April 2020, settling at $94.41 per barrel. The geopolitical risk premium that had been embedded in oil prices for weeks began to unwind rapidly. The ceasefire remains fragile—by Thursday there were reports of continued violations, and the Strait had not yet fully reopened—but markets chose to focus on the direction of travel rather than the details of implementation.

Macro Backdrop: Hot CPI, Soft Core, and the Fed’s Balancing Act

The March Consumer Price Index report, released Friday, provided a complex but ultimately market-neutral data point. Headline CPI rose 0.9% month-over-month, lifting the annual rate to 3.3%—a two-year high, up sharply from 2.4% in February—driven almost entirely by a 10.9% surge in energy costs, with gasoline prices jumping 21.2% and accounting for nearly three quarters of the monthly all-items increase. This reflects the direct pass-through of the Iran war’s oil shock into consumer prices. However, the crucial signal for the Federal Reserve was core CPI, which excludes volatile food and energy prices: core rose just 0.2% month-over-month and 2.6% year-over-year, below expectations and broadly consistent with the Fed’s underlying inflation trajectory. Markets showed little reaction to the report, with equity futures holding gains and Treasury yields moving modestly. The consensus interpretation is that the energy-driven headline spike is a geopolitically induced transitory shock rather than a structural inflation acceleration—one that is already beginning to reverse as oil prices retreat.

The Federal Reserve’s next meeting is scheduled for April 28–29. With one rate cut penciled in for 2026 and the benchmark rate held at 3.50%–3.75%, the ceasefire’s impact on energy prices—if sustained—could meaningfully improve the inflation outlook heading into that meeting, though the central bank is unlikely to move preemptively on incomplete data. Q1 earnings season also kicked off this week, and management commentary on margin pressures from energy costs and tariffs will be closely watched.

Domestic Equities

The sector rotation this week was as dramatic as any point in the year, and it told a clear story: the unwind of the geopolitical risk premium drove a powerful reversal of the trends that had dominated Q1. Communication Services led all sectors with a gain of 5.89%, followed by Consumer Discretionary at +5.81%, Information Technology at +4.82%, and Industrials at +4.69%. These are precisely the sectors that had suffered most during the war-driven risk-off period, and their strong weekly performance reflects investors returning to cyclical and growth exposures as the ceasefire reduced tail risk. Materials gained 3.51%, Real Estate rose 2.93%, Financials added 2.50%, and Utilities advanced 1.28%.

Energy was the notable exception, declining 4.07% on the week as oil prices fell sharply on the ceasefire news. This is the mirror image of the preceding weeks, when Energy was the only sector posting consistent gains. Despite the weekly pullback, the sector retains a commanding year-to-date lead at +28.06%, underscoring the magnitude of the oil-driven move that preceded this week’s reversal. Consumer Staples gained a modest 0.48% and Health Care added 0.36%, the two most defensive sectors again lagging in a risk-on environment.

The equal-weighted S&P 500 rose 1.83%, underperforming the cap-weighted index by roughly 175 basis points, suggesting that large-cap names—particularly in technology and communication services—drove a disproportionate share of the weekly gain. Growth outperformed value across all capitalization tiers: Russell 1000 Growth returned 3.79% versus 2.94% for Russell 1000 Value. Small caps had an excellent week, with the Russell 2000 gaining 3.99% and now solidly positive at +6.33% year-to-date. The Russell Micro Cap advanced 4.06% and is up 7.51% for the year.

International Equities

International equity markets delivered some of the strongest returns of the week, with emerging markets leading global performance in a striking reversal. The MSCI EM surged 7.45% on the week and is now up 10.74% year-to-date, as oil-importing emerging economies responded enthusiastically to the prospect of lower energy costs from a ceasefire-driven supply restoration. India was a standout, advancing 7.07% on the week as it recovered from a period of significant underperformance; the MSCI India Domestic index remains down 9.41% year-to-date but the weekly rebound suggests investors are beginning to revisit valuations in a lower oil price environment. MSCI China gained 3.20%.

Developed international markets also performed strongly. The MSCI EAFE gained 4.44% on the week and has now extended its year-to-date outperformance over U.S. large caps to a meaningful margin, up 6.25% versus the S&P 500’s -0.07%. Germany rose 4.37% and the UK added 3.54%, while Japan gained 3.05% and is now one of the best-performing major markets of the year at +8.85% year-to-date. The MSCI ACWI advanced 4.14%, and the MSCI World gained 3.70%. International diversification has been one of the most rewarding portfolio decisions of 2026, and this week reinforced that theme emphatically.

Fixed Income

Fixed income markets were broadly positive on the week, though gains were modest relative to equities as the risk-on environment reduced safe-haven demand. The Bloomberg U.S. Aggregate Bond Index advanced 0.33%, pushing its year-to-date return to a positive +0.29%, while the Bloomberg Global Aggregate Float Adjusted index gained 0.93% and is now up 0.16% for the year. Corporate bonds led, with the Bloomberg U.S. Corp Bond index rising 0.46% on tightening credit spreads. U.S. Treasuries and Agency debt were marginally positive. The muted but constructive fixed income performance, alongside strong equity gains, reflects a shift in the macro narrative from fear of stagflation toward cautious optimism that the energy shock may be resolving, taking with it the most acute inflationary threat.

Alternatives & Commodities

Bitcoin staged an impressive recovery, surging 9.20% on the week and returning its month-to-date figure to +7.92%, though the year-to-date loss remains substantial at -16.34%. The cryptocurrency appeared to benefit from renewed risk appetite and the broader improvement in investor sentiment following the ceasefire announcement. Gold advanced a more measured 2.30%, extending its year-to-date gain to +10.28% and its twelve-month return to a remarkable +50.67%. The continued strength of gold even as the most acute geopolitical risk receded speaks to the depth of structural demand—central bank purchasing, inflation hedging, and currency diversification—that extends well beyond the current conflict. Real estate investment trusts had an excellent week, with the FTSE NAREIT Composite gaining 3.26%, bringing its year-to-date return to +8.79%, as lower energy costs and the improved growth outlook supported property valuations.

Looking Ahead

Markets enter the week of April 13 with momentum, but also with important unresolved questions. The ceasefire, while market-moving, remains fragile: Iran has yet to fully implement the Strait of Hormuz reopening, the two-week cooling-off period is finite, and peace talks in Islamabad face significant structural obstacles. Any deterioration in the diplomatic process could reverse this week’s risk-on move swiftly. Oil prices, while down sharply, remain well above pre-conflict levels at approximately $94 per barrel, and the March CPI report confirmed that the war’s inflationary effects have already flowed through to consumers.

Q1 earnings season will increasingly dominate the market narrative in the weeks ahead. With the S&P 500 having recovered to near flat on the year, valuations are less distressed than they were at the recent trough, which raises the bar for earnings to sustain the rally. Investors will focus on whether companies can provide constructive forward guidance despite the headwinds of elevated energy costs through most of Q1, ongoing tariff pressures on input costs, and the broader demand uncertainty created by months of geopolitical turbulence. The Federal Reserve’s April 28–29 meeting will also be closely watched, with markets assessing whether the ceasefire’s impact on the energy inflation outlook provides the Fed with any additional flexibility on its rate path.

Source: Morningstar. Market data as of April 10, 2026. Economic and news data sourced from CNBC, CBS News, NBC News, BLS, Al Jazeera, and FinancialContent. Past performance is not indicative of future results. This commentary is for informational purposes only and does not constitute investment advice.